from The Mel K Show:

TRUTH LIVES on at https://sgtreport.tv/

by JD Rucker, Discern Report:

There’s a scene in the Liam Neeson movie “Taken” where he’s on the phone with his daughter. Men are there to kidnap her and she’s a world away from him in Europe. As a former intel agent, he knows what’s going to happen and realizes there’s no way to stop it. As much as he’d love to come up with a way for his daughter to escape or fight off the assailants, he knows the best thing he can do is to prepare her by telling her the truth.

“Now, the next part is very important — they’re going to take you,” he said.

from Moonbattery:

Let’s pretend for a minute that there is something wrong with the weather. If we let Democrats bankrupt the country by spending $50 trillion on climate worship virtue signaling, how much weather improvement do we get for the money?

Most readers know the short answer: none. Senator John Kennedy pries the long answer out of Biden Regime apparatchik David Turk of the Department of Energy (which should be abolished):

by Joe Wolverton, II, J.D., The New American:

“He has erected a multitude of New Offices, and sent hither swarms of Officers to harrass our people, and eat out their substance.” — Declaration of Independence

The IRS, the U.S. Postal Service, the EPA, the Department of Health and Human Services, and more than 100 other federal agencies (none of which operate under the aegis of the Department of Defense) have “spent $3.7 billion on guns, ammunition, and military-style equipment,” according to a new report on the arming of the bureaucracy.

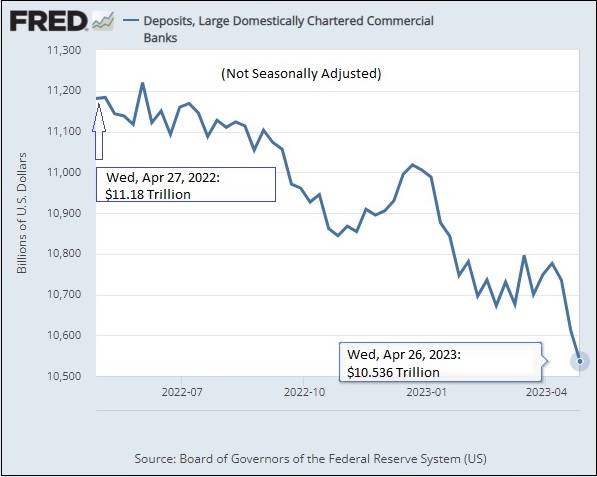

by Pam Martens and Russ Martens, Wall St On Parade:

Since the banking crisis began making headlines at expensive media real estate, the narrative has been that deposits are fleeing the small commercial banks and flooding into the biggest banks that are perceived as too-big-to-fail and thus offer a safer venue for deposits.

Because these mega banks are the same ones that the Fed has been bailing out since the financial crisis of 2008, that narrative requires believing that our fellow Americans are dumber than a stump.

by Michael Snyder, The Economic Collapse Blog:

This new economic downturn is starting to bite, and we are starting to see signs of severe pain all over the nation. In fact, unless you are independently wealthy, you are likely feeling pain too. The cost of living has risen to extreme oppressive levels, and this has happened at a time when close to two-thirds of the country was already living paycheck to paycheck. As a result, many Americans are having their finances stretched to the breaking point, and millions of them are reaching out for help. For example, on Saturday morning the line of people waiting for assistance at one of Boston’s largest food pantries “stretched the length of two football fields”…

by Harvey Organ, Harvey Organ Blog:

GOLD CLOSED UP $8.70 TO $2025.60 AS INVESTORS DEMAND PHYSICAL DELIVERY FROM THE MASSIVE SHORTS ON FRIDAY//SILVER WAS DOWN 7 CENTS TO $25.57//PLATINUM CLOSED UP $17.10 TO $1079.30//PALLADIUM CLOSED UP $51.10 TO $1555.50//ANDREW MAGUIRE: A MUST VIEW TAPE//ALSO DR DANIEL LACALLE: A MUST READ!//UKRAINE VS RUSSIA: THE CRAZY UKRANIANS ARE FIRING ON THEIR NUCLEAR FACILITY//COVID UPDATES//DR PAUL ALEXANDER/VACCINE IMPACT/SLAY NEWS/EVOLE NEWS//IN USA: HUGE RUN ON THE BANKS WITH 360 BILLION DOLLARS LEAVING BANK DEPOSITS FOR MONEY MARKETS//CREDIT CARD USE INCREASE AGAIN IN DRAMATIC FASHION AS MANY AS MAXED OUT//CALIFORNIA DEFAULTS ON PANDEMIC FUNDS ISSUED BY THE FEDS//TYSON FOODS, LARGEST FOOD PRODUCER IN THE USA SHOWS A LOSS IN LASTEST QUARTER/

GOLD CLOSED UP $8.70 TO $2025.60 AS INVESTORS DEMAND PHYSICAL DELIVERY FROM THE MASSIVE SHORTS ON FRIDAY//SILVER WAS DOWN 7 CENTS TO $25.57//PLATINUM CLOSED UP $17.10 TO $1079.30//PALLADIUM CLOSED UP $51.10 TO $1555.50//ANDREW MAGUIRE: A MUST VIEW TAPE//ALSO DR DANIEL LACALLE: A MUST READ!//UKRAINE VS RUSSIA: THE CRAZY UKRANIANS ARE FIRING ON THEIR NUCLEAR FACILITY//COVID UPDATES//DR PAUL ALEXANDER/VACCINE IMPACT/SLAY NEWS/EVOLE NEWS//IN USA: HUGE RUN ON THE BANKS WITH 360 BILLION DOLLARS LEAVING BANK DEPOSITS FOR MONEY MARKETS//CREDIT CARD USE INCREASE AGAIN IN DRAMATIC FASHION AS MANY AS MAXED OUT//CALIFORNIA DEFAULTS ON PANDEMIC FUNDS ISSUED BY THE FEDS//TYSON FOODS, LARGEST FOOD PRODUCER IN THE USA SHOWS A LOSS IN LASTEST QUARTER/

by TheDarkMan, The Duran:

Cheques (or checks in American parlance) have been with us a long time. Although they take a while to clear, they are safer to use than cash, especially for large purchases. At one time, ordinary people, especially women, would not be issued with chequebooks by their banks. Cheques have two big advantages over cash. If you sign a cheque for a thousand dollars then lose it or it is stolen, you simply put a stop on it with your bank whereas if you lose cash, it’s usually gone forever. Cheque payments can also be traced, so again, they are safer than cash.

by Martin Armstrong, Armstrong Economics:

A lot of people somehow think that the move to Digital Currency is a completely new monetary system, It is targeted to eliminate cash transactions so everything is taxable and nothing can be hidden from our overlords. If we look at commerce in the United States during 2022, 82% of all transactions were digital – Debit cards (20 percent), credit cards (30 percent), and digital wallets 32 percent. That was e-commerce.

from Stew Peters Network:

TRUTH LIVES on at https://sgtreport.tv/

by Matt Agorist, The Free Thought Project:

(FEE) — The Federal Housing Finance Agency (FHFA) has begun to implement new rules for mortgage borrowers. The result of these new rules is that, everything else held constant, some borrowers with relatively higher credit ratings who make larger down payments on houses will pay higher fees than they did before. Likewise, some borrowers with worse credit ratings who make smaller down payments will pay less.