from 21st Century Wire:

Imagine this: It’s payday but before the money reaches your account, someone else has already decided what you’ll spend your money on — one third of your paycheck on housing, one third on food (only plant and insect protein allowed), 10% on transportation (with little allowance for gas), 10% on a mandatory pension plan (mostly allocated to government bonds) and the remaining 14% on clothing, alcohol and pharmaceuticals in state-licensed shops. Spending outside of these allocations comes with huge markups and, as if this isn’t bad enough, saving is impossible as this money comes with an expiration date: after three months, it simply disappears from your account.

TRUTH LIVES on at https://sgtreport.tv/

This dystopian world is closer than you think. Central bank digital currencies, or CBDCs, could make it a reality. CBDCs are an attempt to duct-tape the failing monetary system back together, and in the process provide the State with nearly unlimited control over the financial system, and thus our spending habits and the way we lead our lives.

In this article, I explain the motivation for governments pursuing the CBDC programs, why it is one of the greatest threats to our freedoms today and what steps you can take to limit its impact on you and your family.

All Fiat Fails

Fiat currency is the only form of money most of us have known throughout our lives. It may seem natural and inevitable but when we look a bit farther into history, we find out that it’s anything but that; in fact, fiat currency seems more like a dead end in the context of monetary history.

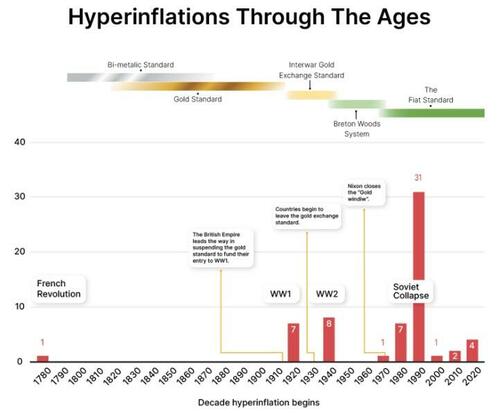

For thousands of years, mankind has converged to gold and silver as the dominant form of money. Only for the past 100 or so years have we diverged from this historic trend. And the results have been disastrous. As Joakim Book noted in his recent article on hyperinflations, 61 out of the 62 documented cases of hyperinflation happened in the past 100 years — in the era of fiat money, when the ties to precious metals were cut.

Source: Joakim Book: “What Is Hyperinflation And How Does It Happen?”

Even when a currency isn’t undergoing hyperinflation, people and economies still suffer. A “regular” inflation in single or double digits is sufficiently destructive through its cumulative effect. Per my own calculations, inflation of 2% — a common inflationary target that many central banks aim for — halves the purchasing power of the given currency in about 35 years, while the recent inflation rates around 10% manage to do so in seven years.

Source: Author

In short, fiat currencies either die quickly or evaporate slowly. In the end, they all fail.

Why CBDCs Now?

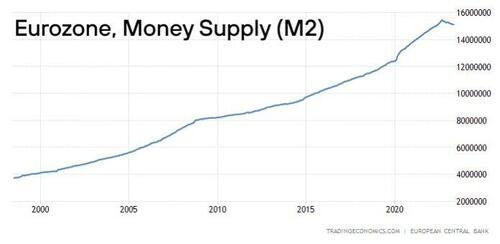

Some policy makers are aware of this intrinsic nature of fiat currencies, and try to duct-tape their monetary systems through a reform — instead of letting the currency die in a spectacular hyperinflationary episode, they euthanize it instead and replace it with another fiat currency. This is in essence what happened across Europe at the turn of the century, when the euro was rolled out: smaller currencies suffering from high inflation rates (such as the Italian lira, Greek drachma and Spanish peseta) were overhauled into a new fiat currency that, at least until recently, allowed the establishment to kick the can down the road via rampant money printing and ballooning debts, as demonstrated in the chart below.

The euro money supply (M2 aggregate) has nearly quadrupled since the turn of the century, from almost 4 trillion euros in 1999 to almost 16 trillion euros in 2023. Source: Trading Economics.

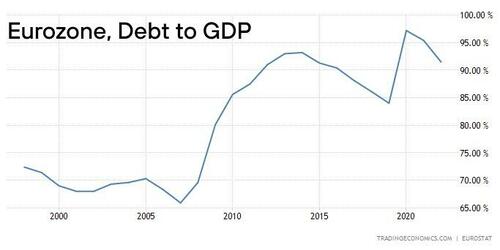

The eurozone members’ government-debt-to-GDP ratio has risen from below 70% in 2000 to more than 90% in 2023. Most of the eurozone member countries no longer fulfill the debt-to-GDP Maastricht criteria that states the government’s debt shouldn’t exceed 60%. Source: Trading Economics.

The situation looks strikingly similar all around the world: money supplies inflating, purchasing power steadily declining, debt levels ballooning. The outcomes are the same, because the cause is the same: monetary systems based on currencies that can be printed at will are failing.

Some governments reform their currency in a very naive way, by simply removing a couple of zeros from the existing denominations and calling it a day. A typical example of such a reform was the 2016 overhaul of the Belarusian ruble, during which the government simply scratched off four zeros from the currency.

Using central bank digital currencies is a slightly more sophisticated attempt at reforming failing monetary systems, though they won’t change fiat currencies in any fundamental way. If anything, CBDCs are putting more power in the hands of governments and will likely lead to an even greater erosion of the purchasing power of ordinary citizens.

The Ultimate Corruption of Money

One of the most efficient ways to enslave a society is to destroy a currency’s two main functions: its roles as a store of value and as a medium of exchange.

Fiat currencies already ceased working as a reliable store of value a long time ago, through an intentional policy of permanent inflation. Preventing citizens from saving independently and incentivizing society to go into ever-deeper debts leads to a greater dependence on the state and its policies. Fiat currencies lead to debt slavery, and CBDCs won’t reverse this trend.

CBDCs As Store of Value

To understand why CBDCs will likely lead to a much greater erosion of the store-of-value function of money, let’s look at how today’s financial systems operate. Let’s take the U.S. banking system as an example (most financial systems around the world are structured in pretty much the same way).

The Federal Reserve, the U.S. central banking system, regulates the financial system and executes monetary policies. During and after the 2008 financial crisis, the Fed implemented a very loose monetary policy with interest rates near zero to stimulate the economy. This is where we get to a second crucial element of the U.S. financial system, in the form of commercial banks. Banks were unwilling to lend out the new inflow of money and instead deposited trillions of dollars with the Fed, as we can see on the chart below. This, in part, limited the effectiveness of the central bank’s policies.

Read More @ 21stCenturyWire.com