by Wolf Richter, Wolf Street:

![]() Complicated times for the dollar. The Chinese Renminbi, a distant also-ran, loses ground.

Complicated times for the dollar. The Chinese Renminbi, a distant also-ran, loses ground.

The last three years were complicated for the dominant reserve currency. At first there was the Fed’s $5-trillion money-printing orgy and interest-rate repression. Then there was raging inflation, which the Fed brushed off as “transitory.” Through this period, the dollar fell against other currencies. But then the Fed got religion and began to tighten: since March 2022, it has hiked rates by 425 basis points, accompanied over the past six months by $414 billion in QT so far. As a result, the dollar bounced off and shot higher against other currencies, particularly the euro and the yen – the #2 and #3 reserve currencies. TRUTH LIVES on at https://sgtreport.tv/

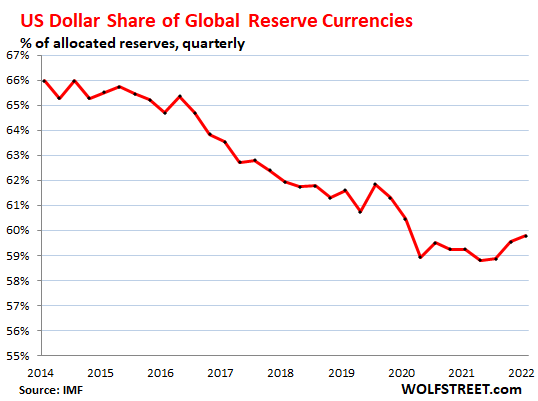

At the end of Q3, the share of US-dollar-denominated foreign exchange reserves rose to 59.8%, the third quarter in a row of increases, and the highest since Q3 2020, according to the IMF’s new COFER data on reserve currencies. Since the end of 2021, the share of the dollar rose by nearly 1 percentage point.

But this increase came off a 26-year low at the end of 2021. Note that this does not include the dollar-denominated assets on the Fed’s balance sheet, but only dollar-denominated assets held by foreign central banks and foreign official institutions:

These foreign central banks and official institutions also hold assets denominated in other currencies. And all those assets combined make up the total global foreign exchange reserves, which amounted to $11.6 trillion in all currencies when expressed in USD, according to the IMF’s COFER data; 59.8% were dollar-denominated assets.

The remaining 40.2% were assets denominated in other currencies, primarily the euro, and a bunch of also-rans, whose value were then translated into USD.

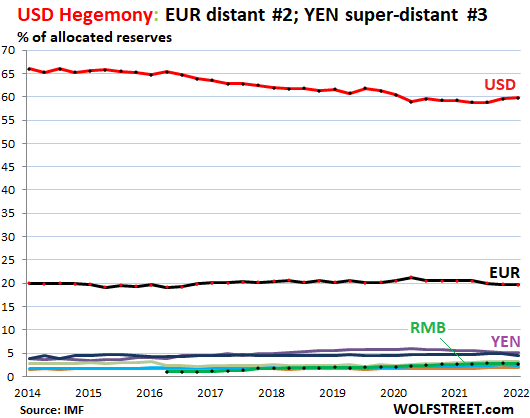

The other major reserve currency, and the also-rans.

The euro is the second largest reserve currency. The Eurozone encompasses 19 countries with a population of 340 million people. Over two decades ago, when the euro was being promoted to Europeans, they often talked about “parity” of the euro with the dollar on all levels: as global reserve currency, as trading currency, and as financing currency. This reserve currency parity made progress until the Euro Debt Crisis brought to light the euro’s structural weakness. And that put an end to this parity talk.

Since then, the euro has had a share of about 20% of global reserve currencies (in Q3, 19.7%), about as large as all also-rans combined. But it was far below the dollar (black line, red dots in the chart below).

The yen (purple line at the top of the colorful spaghetti at the bottom in the chart) had a share of 5.3%. It became the #3 reserve currency in 2018, when its share surpassed that of the British pound.

The British pound, the #4 reserve currency, had a share of 4.6% (blue line just under the yen in the spaghetti).

The Chinese renminbi, the #5 reserve currency, dipped to a share of 2.8% in Q3 — only 2.8%, despite the huge size and global interconnection of China’s economy! Given the capital controls still in place, and other issues, it seems central banks are leery of RMB-denominated assets and are in no hurry to pile them on, despite years of predictions that they would. Folks that expect the Renminbi to overtake the US dollar as reserve currency will have to have enormous patience (green line with black dots near the very bottom).

The other currencies in the spaghetti: Canadian dollar (2.4%), Australian dollar (1.9%), and Swiss franc (0.23%). There are other currencies, each of which has such a small share that it doesn’t matter.

You can have a large trade surplus and a large reserve currency just fine.

The Eurozone has had a large trade surplus with the rest of the world in recent years – particularly with the US. This demonstrates that an economy with a trade surplus can also have one of the top reserve currencies, thereby debunking the outdated theories that the country with a large reserve currency must have a large trade deficit.

But having the dominant reserve currency encourages the US to run up its gigantic twin-deficits: The US government deficits that have produced the incredibly spiking public debt; and the ballooning trade deficit, powered by Corporate America’s three-decade search of cheap labor. Both of these deficits would be more expensive to fund if the dollar were not the dominant reserve currency.

Dollar’s share gains in 2022 may be over: exchange rates and foreign exchange reserves.

Since the end of Q3, the ECB hiked rates and shed a huge €850 billion in assets, and the euro reacted, recovering some against the dollar. And the Bank of Japan made noises in that direction, and the yen bounced.

The values of foreign exchange reserves denominated in euros, yen, British Pound, renminbi, and other currencies are translated into dollar figures at the current exchange rate, so that they can be summed and compared.

For example, within the IMF’s data, the value of Japan’s official holdings of euro-denominated assets is expressed in dollars at the current EUR-USD exchange rate.

The exchange rate between the USD and other reserve currencies impacts the magnitude of the non-USD assets. To stick with our example, the magnitude, expressed in dollars, of the euro-denominated assets held by Japan fell as the euro’s exchange rate fell against the dollar.

So the increase in the share of the USD since the end of 2021 may have run its course because the plunge of the euro and yen have ended, and both currencies have bounced since the end of Q3.

Overall, over the past two decades, the exchange rates of the major currency pairs have bounced up and down within a fairly wide band, as shown by the Dollar Index [DXY], which tracks the exchange rates of the dollar against the euro, yen, British pound, Canadian dollar, Swedish krona, and Swiss franc. The DXY is dominated by the euro and yen.