by Pam Martens and Russ Martens, Wall St On Parade:

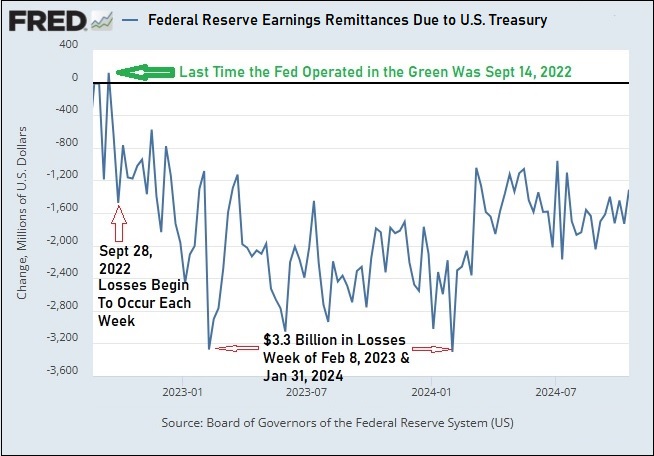

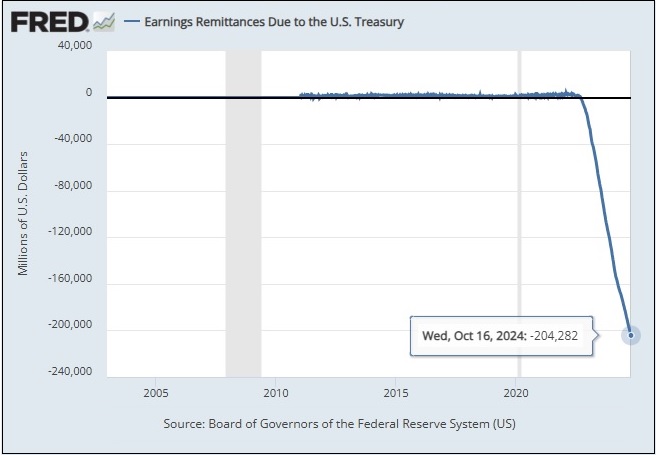

According to its own FRED data, the last time the central bank of the United States – the Federal Reserve – operated in the green was September 14, 2022, more than two years ago. Since then, it has been consistently losing over $1 billion a week with its cumulative operating losses now topping $204 billion as of the last reporting by the Fed on October 16, 2024.

Operating losses of this magnitude are unprecedented at the of Fed, which was created in 1913.

TRUTH LIVES on at https://sgtreport.tv/

If a publicly-traded company had been bleeding operating losses of more than $1 billion a week for more than two years, there would very likely be a change of leadership at the top. But Fed Chair Jerome Powell is no ordinary mortal. He survived the worst trading scandal in the Fed’s history – even after his own trading conduct came into question.

These losses at the Fed are operating losses – where expenses exceed earnings. They are not to be confused with the unrealized losses on the Fed’s underwater debt securities that the Fed holds on its balance sheet, which it does not mark to market.

The Fed is experiencing these operating losses because the interest it is earning on its $6.6 trillion portfolio of debt securities that it acquired through its Quantitative Easing (QE) operations is less than the overly generous interest payments it is making to banks. These payments include the 4.90 percent interest the Fed is paying to the megabanks on Wall Street (and other Fed member banks) for the reserves they hold with the Fed. This morning, the yield on the benchmark 10-year U.S. Treasury note is just 4.13 percent. That yield hasn’t climbed above 4.50 percent for more than four months. So why is the Fed continuing to pay out the overly generous rate of 4.90 percent interest on reserves to the banks it supervises when it’s bleeding losses?

Is the Fed blatantly subsidizing bank profits while some of these same megabanks charge double digit interest rates to consumers on their credit cards? (See, for example: While JPMorgan Chase Was Getting Trillions of Dollars in Loans at Almost Zero Percent Interest from the Fed, It Was Charging Americans Hit by the Pandemic 17 Percent on their Credit Cards.)

The Fed is also paying out the overly generous rate of 4.80 percent on its reverse repo operations with giant mutual fund companies – many of which are owned by the megabanks on Wall Street. And, the Fed is paying a ridiculous 6 percent dividend to member shareholder banks with assets of $10 billion or less. Banks with assets above $10 billion receive the lesser of 6 percent or the yield on the 10-year Treasury note at the most recent auction prior to the dividend payment.

U.S. taxpayers have good reason to be alarmed by the Fed’s ongoing operating losses. That’s because when the Fed is operating in the green, the Fed, by law, turns over excess earnings to the U.S. Treasury – thus reducing the amount the U.S. government has to borrow by issuing Treasury debt securities. According to Fed data, between 2011 and 2021, the Fed’s excess earnings paid to the U.S. Treasury totaled more than $920 billion.

The loss of remittances from the Fed means that the U.S. government will go deeper into debt, putting a heavier tax burden on the U.S. taxpayer and raising the risk of another credit rating agency downgrade of U.S. sovereign debt.

Another problem at the Fed is that instead of being a beacon for pristine accounting practices, it is engaging in creative accounting according to experts. A January 31 paper by Paul H. Kupiec and Alex J. Pollock published by the American Enterprise Institute explains in stark detail why the Fed has negative capital under GAAP accounting. The researchers write:

Read More @ WallStOnParade.com