from Schiff Gold:

The Comex report for last month correctly identified a potential big move in silver while the same report two months ago preceded a massive up move for the price of gold. The data this month is not as obvious or compelling, but it is clear the stress on the Comex continues to build.

The CME Comex is the Exchange where futures are traded for gold, silver, and other commodities. The CME also allows futures buyers to turn their contracts into physical metal through delivery. You can find more detail on the CME here (e.g., vault types, major/minor months, delivery explanation, historical data, etc.).

TRUTH LIVES on at https://sgtreport.tv/

The data below looks at contract delivery where the ownership of physical metal changes hands within CME vaults. It also shows data that details the movement of metal in and out of CME vaults. It is very possible that if there is a run on the dollar, and a flight into gold, this is the data that will show early warning signs.

Gold

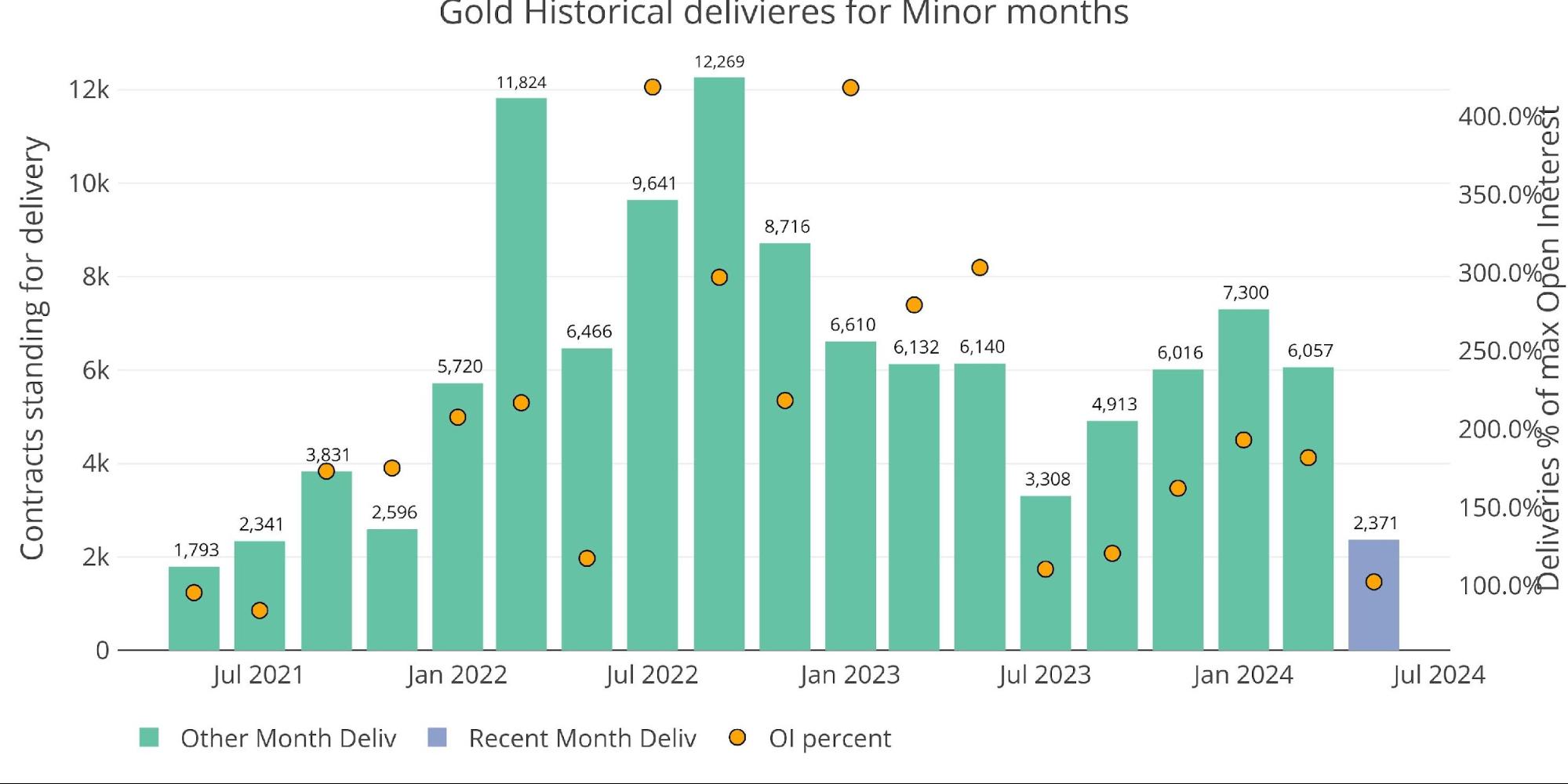

May is a minor delivery month in gold. The delivery amount this month was actually quite small. The 2,371 contracts were the smallest delivery volume since July 2021.

Figure: 1 Recent like-month delivery volume

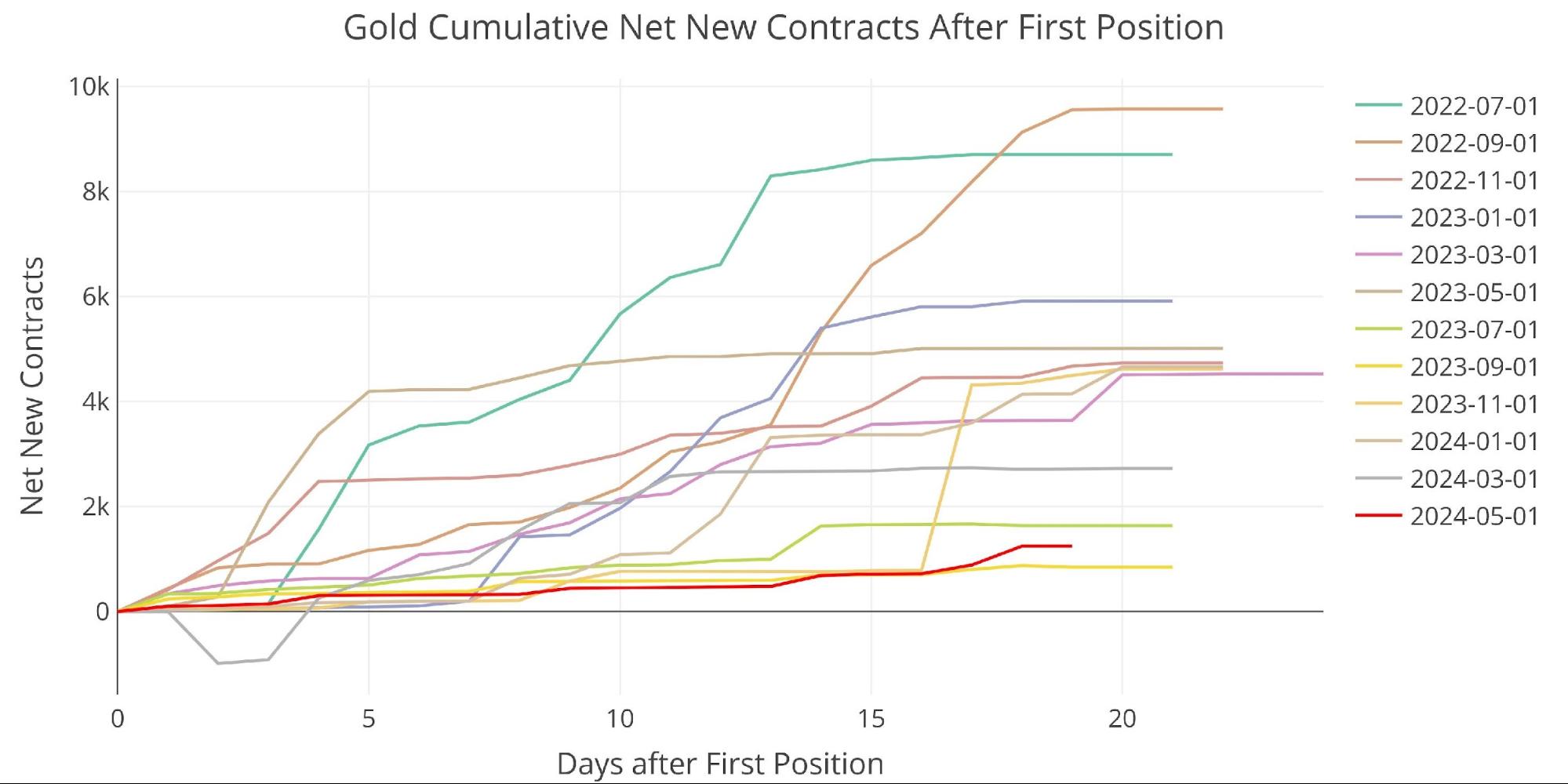

Net new contracts are the main reason for the low delivery volume. Contracts delivered after the delivery window started is one of the lowest in recent history.

Figure: 2 Cumulative Net New Contracts

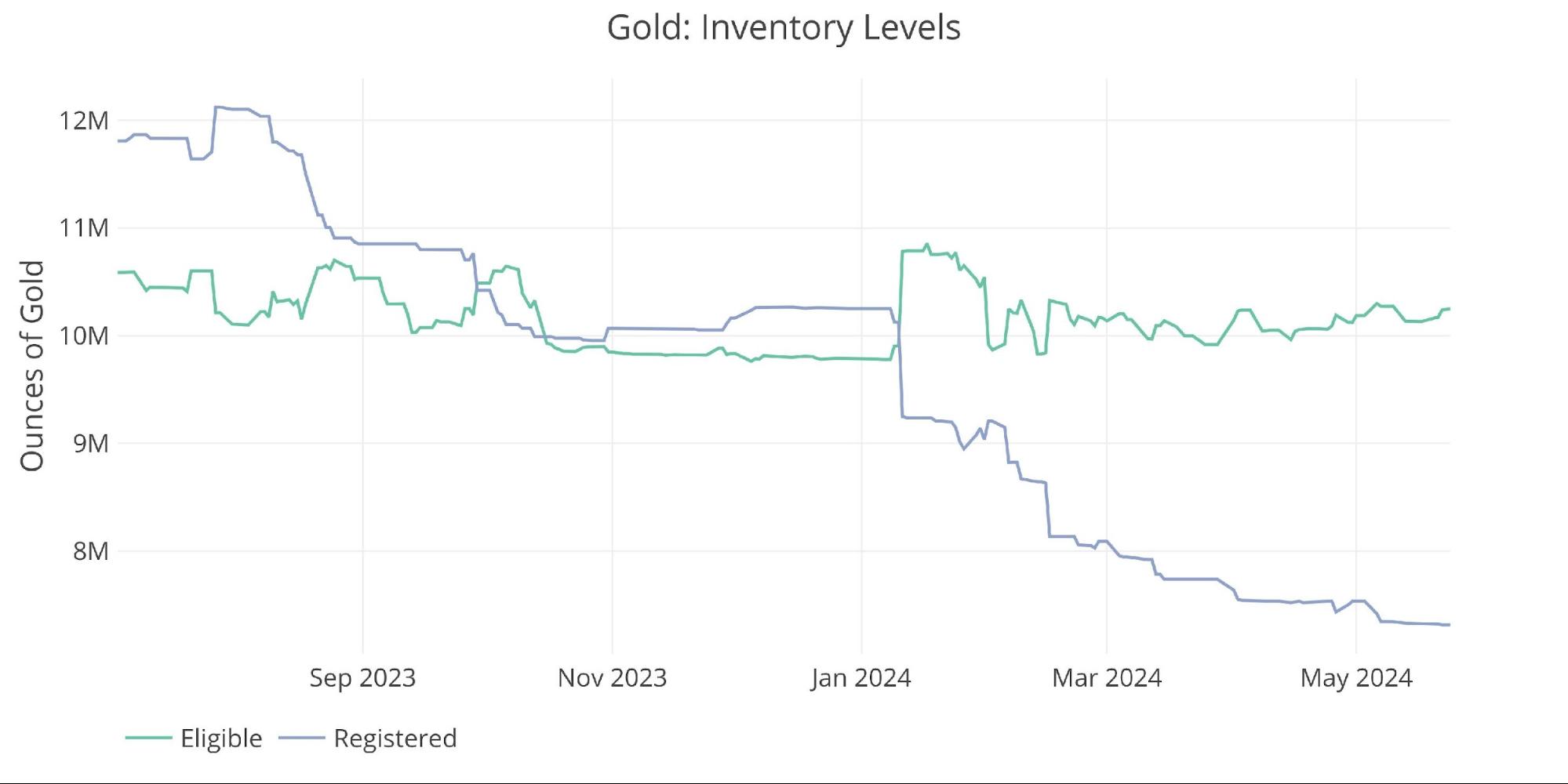

Inventory levels have been very stable the last few months with just a slow drop in Registered.

Figure: 3 Inventory Data

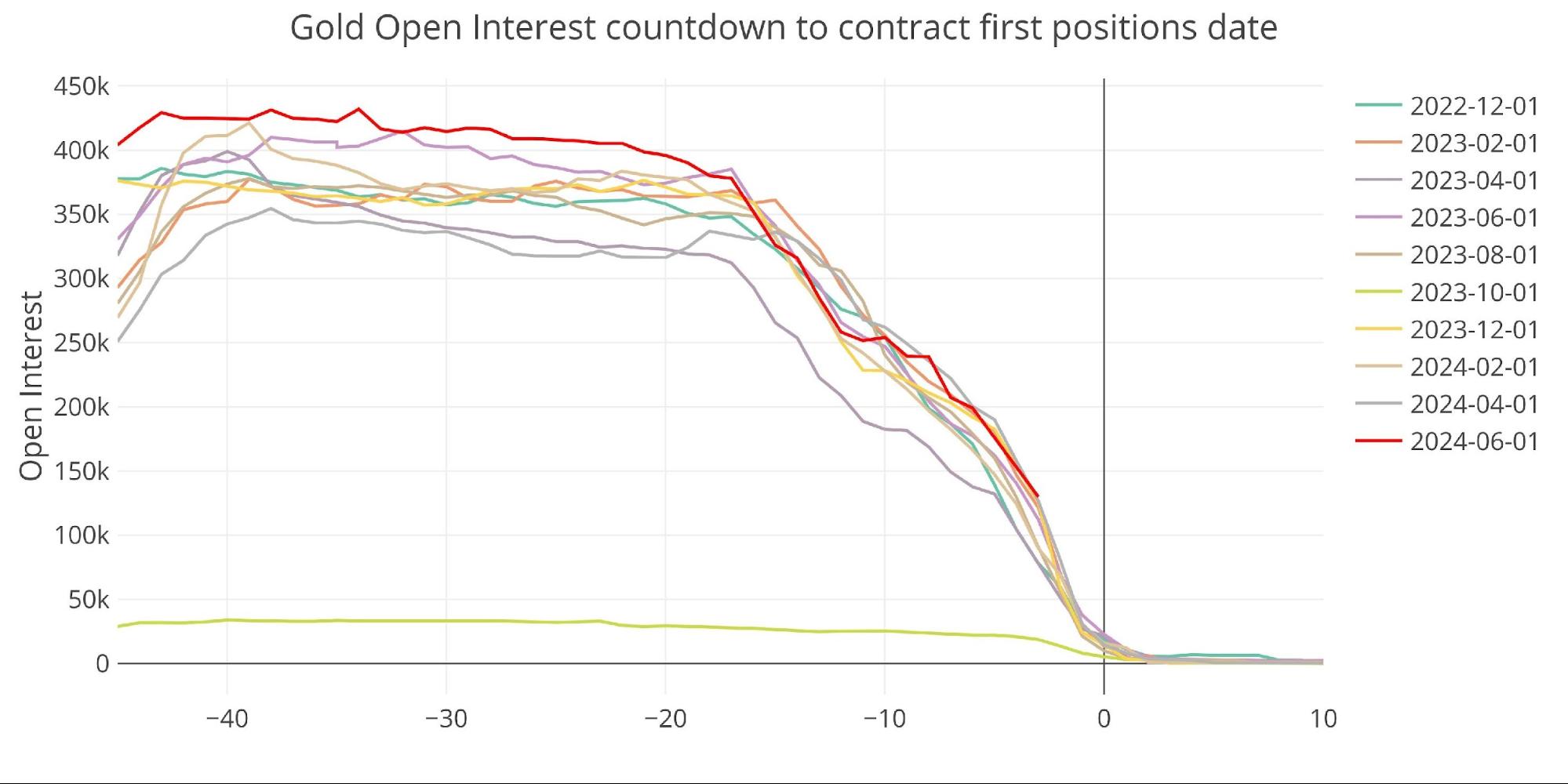

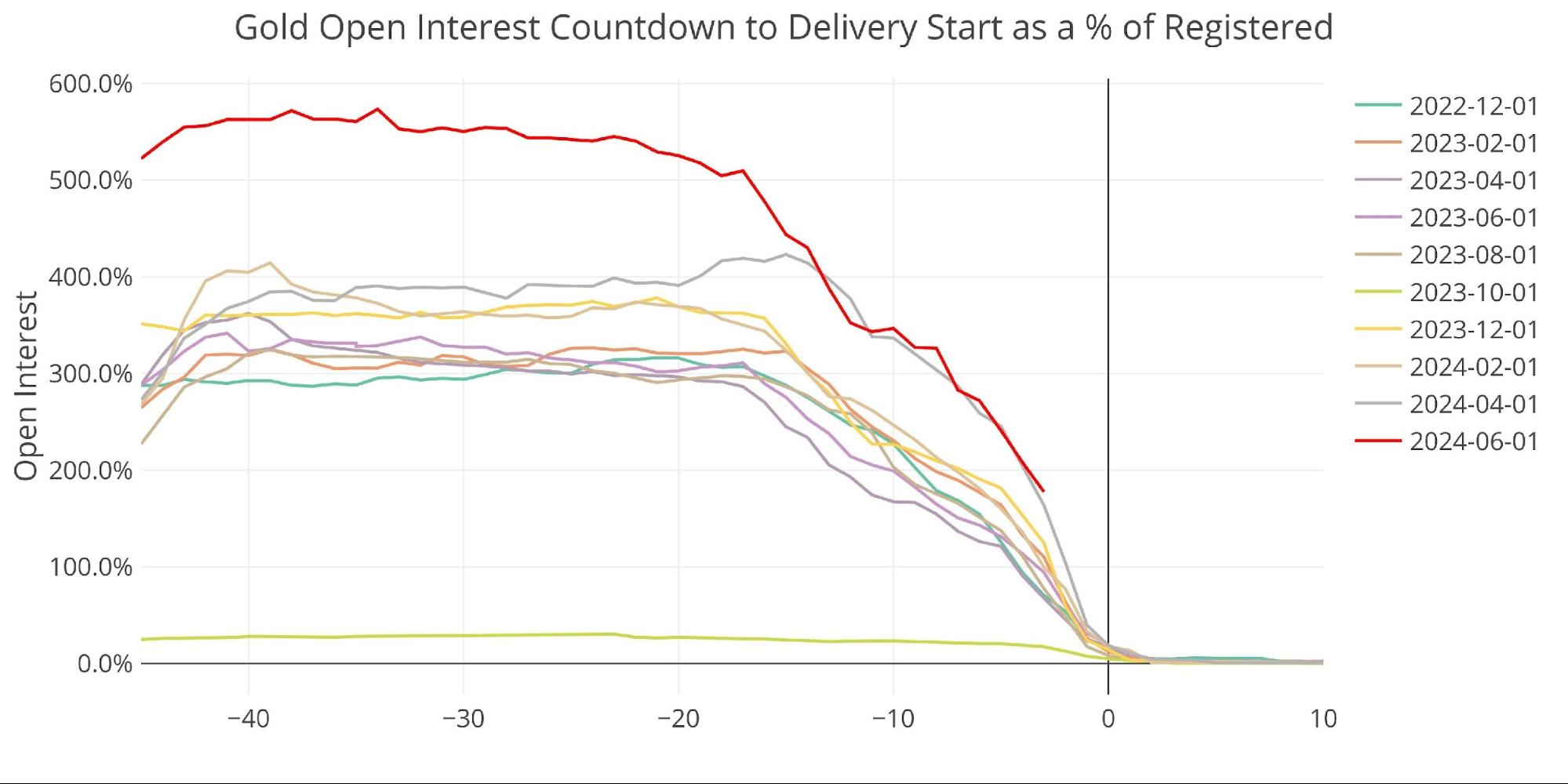

Heading into the major delivery month of June shows Open Interest is much higher than average.

Figure: 4 Open Interest Countdown

This can be seen more clearly on a relative basis where the current level of contracts relative to Registered metal is the highest in recent months.

Figure: 5 Open Interest Countdown Percent

Silver

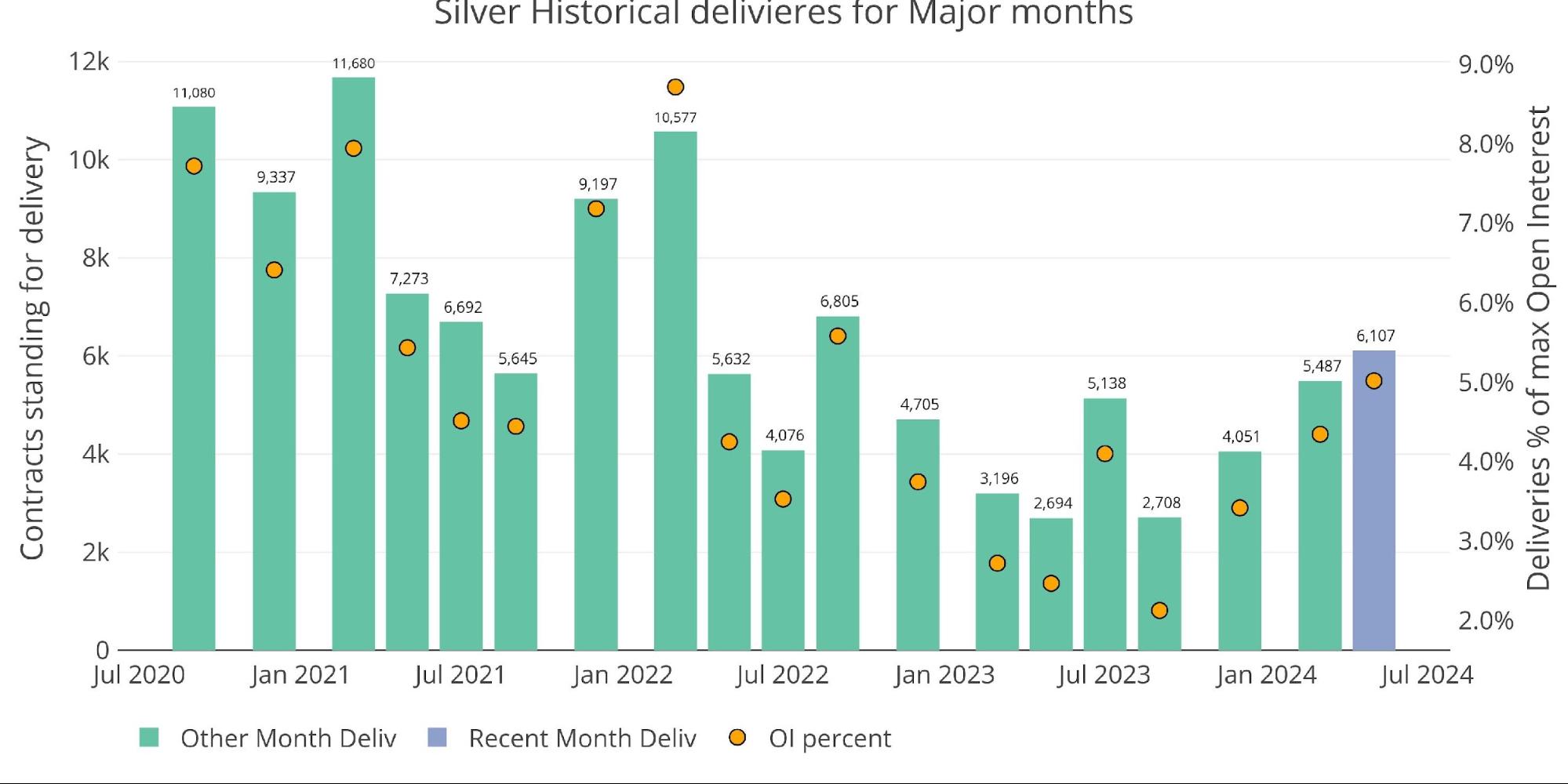

May delivery is a major delivery month for silver. Delivery volume reached the highest since September 2022 with 6,107 contracts delivered.

Figure: 6 Recent like-month delivery volume

Unlike past months, this was not driven by net new contracts which represented only 500 of the total contracts delivered.