by Pam Martens and Russ Martens, Wall St On Parade:

There is a battle raging between the Wall Street mega banks and their federal banking regulators. The regulators want the mega banks to hold more capital against their high risk trading positions to prevent a replay of the bailouts in 2008 and repo bailouts in the fall of 2019. The mega banks have launched a deceptive ad campaign and public relations battle to thwart that from happening.

The federal regulators’ efforts to raise capital are being undermined by Fed Chairman Jay Powell’s perpetual testimony to Congress that the U.S. banking system is safe and sound and adequately capitalized.

TRUTH LIVES on at https://sgtreport.tv/

Thus far, no member of Congress has thought to question Fed Chair Powell during public hearings as to why the Fed needs a new permanent bailout facility of $500 billion, on top of its century-old Discount Window, if the banking system is adequately capitalized.

The half trillion dollar bailout facility has the benign-sounding name of Standing Repo Facility (SRF). (The Fed always gives a benign-sounding name to the unprecedented bailout facilities it has been perpetually creating since 2008.)

On July 28, 2021, when first disclosing the creation of the SRF, the Federal Reserve made the following unprecedented announcement:

“Under the SRF [Standing Repo Facility], the Federal Reserve will conduct daily overnight repo operations against Treasury securities, agency debt securities, and agency mortgage-backed securities, with a maximum operation size of $500 billion. The minimum bid rate for repos under the facility will be set initially at 25 basis points, somewhat above the general level of overnight interest rates. Counterparties for this facility will include primary dealers and will be expanded over time to include additional depository institutions.”

Primary dealers are decidedly not deposit-taking institutions. The word “dealer” gives this away. They are broker-dealers, meaning their business is the trading of securities, such as stocks, bonds, commodities, and futures. It was never the intent of Congress to make the Federal Reserve the lender of last resort to trading casinos on Wall Street.

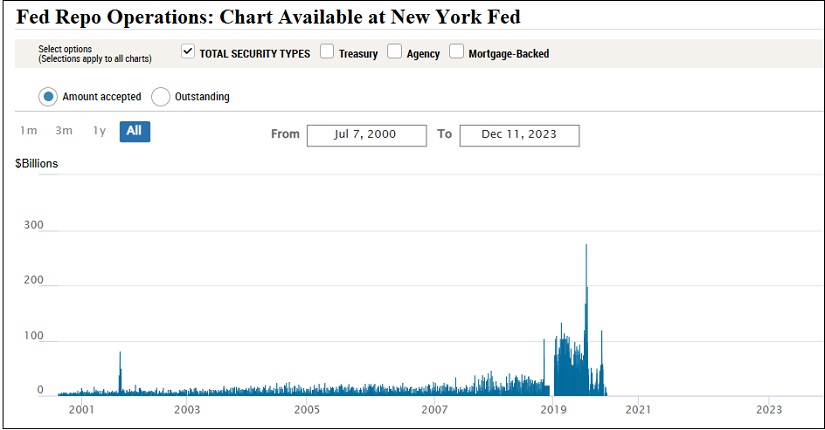

Repos, short for Repurchase Agreements, are overnight loans that are typically made between financial institutions where safe collateral such as short-term Treasury securities are posted to ensure the repayment of the loan. When the Fed has to get involved in the Repo market, it means there is a liquidity crisis of some nature, such as mega banks backing away from lending to each other out of fear of default.

The chart above shows the increasing nature of the Fed’s involvement in the repo market as a bailout facility to the trading houses on Wall Street.

The controlling legislation for the Federal Reserve is the Federal Reserve Act. That legislation makes clear that the Fed is to be the lender of last resort to depository institutions – those taking deposits from individuals and businesses – by making short term loans through its Discount Window. (Depository institutions are worthy of central bank emergency loans because they, in turn, make loans to consumers and businesses to grow the U.S. economy.) In case of a dire emergency, the Fed is also allowed to make short-term loans under emergency lending facilities. The Fed’s establishment of a permanent lending facility to support securities trading on Wall Street shows just how distorted the Fed’s mission has become.

The Fed has also made it possible for the mega banks on Wall Street to now get two bites from the same apple. Each of the mega banks own a primary dealer (securities trading house) as well as a federally-insured bank. The Fed has now made both units eligible to borrow from its Standing Repo Facility.

For example, JPMorgan Chase’s broker-dealer, J.P. Morgan Securities LLP, is a primary dealer with the New York Fed and, thus, automatically eligible to borrow from the Standing Repo Facility. The Fed has also approved JPMorgan Chase Bank, the federally-insured banking unit of JPMorgan Chase, to borrow at its Standing Repo Facility. Two units of the same corporate parent will now be able to tap the daily maximum lending limit set by the Fed, giving the mega bank twice the borrowing capacity.

The chart above from the New York Fed shows that no lending has occurred from the Fed’s repo facility or Standing Repo Facility since the still unexplained mega bank crisis in the last quarter of 2019 through the COVID pandemic crisis of 2020. And yet, the New York Fed has this statement on its website:

“The New York Fed Trading Desk conducts overnight repo transactions under a Standing Repo Facility to support the effective implementation of monetary policy and smooth market functioning. In addition to primary dealers, participants in these transactions include Standing Repo Facility counterparties.”

For insight into whether the New York Fed has actually stopped making its bailout repo loans or just tucked them into a more opaque part of its own plumbing, see our report: Watchdog Report: Fed’s Billions in Emergency Repo Loans to Wall Street Didn’t Go Away in June; They Just Went Dark.

The New York Fed’s insatiable money spigot to the mega banks on Wall Street impacts the U.S. economy because it fuels wealth inequality by enriching the top 10 percent of Americans who own the vast majority of all stocks and bonds in the U.S. It impacts the economy further because it is ballooning the size of the Fed’s balance sheet (which now stands at $7.8 trillion) which the U.S. taxpayer is ultimately on the hook for. It impacts the U.S. economy because it is worsening the bubble that already exists in the stock market, thus making the inevitable bursting of the bubble worse. And it impacts the U.S. economy because these unprecedented bailouts of Wall Street by the Fed undermine the trust the American people have in their central bank and the U.S. banking system. (See here and here.)

Read More @ WallStOnParade.com