by Pam Martens and Russ Martens, Wall St On Parade:

Yesterday, the regulator of the Federal Home Loan Bank system, the Federal Housing Finance Agency (FHFA), released a report on its recommended changes going forward. The report was in response to the questionable conduct of the Federal Home Loan Banks in the leadup to the banking crisis this past spring.

The core mission of the 11 regional Federal Home Loan Banks is to “provide liquidity to their members to support housing finance and community development through all economic cycles.” In short, the Federal Home Loan Banks are supposed to make it possible for banks to provide home mortgages to low-income folks. The banks that failed this spring were engaged in crypto (Silvergate and Signature Bank), providing loans to the super wealthy (First Republic Bank), and in the case of Silicon Valley Bank, it was more of a Wall Street IPO pipeline. (See our report: Silicon Valley Bank Was a Wall Street IPO Pipeline in Drag as a Federally-Insured Bank; FHLB of San Francisco Was Quietly Bailing It Out.)

TRUTH LIVES on at https://sgtreport.tv/

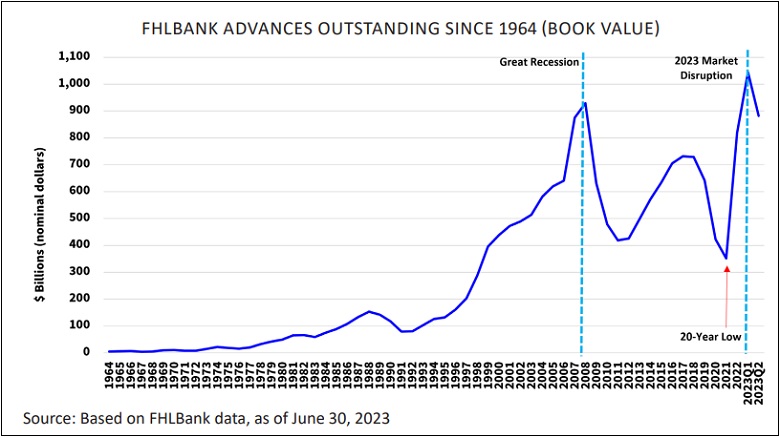

As the chart above, from the report, indicates, one of the shockers is that commercial banks were in such desperate need for cash this past spring that they borrowed more from the Federal Home Loan Banks than they did during the financial crash of 2008 – which was the worst financial crisis since the Great Depression. This suggests that perhaps the severity of this spring’s bank run has been downplayed by federal regulators.

Another troubling revelation in the report is that JPMorgan Chase, the largest bank by both assets and deposits in the U.S., has not repaid the money that First Republic Bank had borrowed from the Federal Home Loan Bank of San Francisco. JPMorgan Chase (with much controversy because it is already the riskiest bank in the U.S.) was allowed by regulators to acquire First Republic Bank when it failed on May 1. The FHFA report notes the following:

“On May 1, 2023, the California Department of Financial Protection and Innovation closed First Republic Bank, which was acquired by JPMorgan Chase. Of the FHLBank advances to First Republic Bank at the time of its acquisition, $26.4 billion remained outstanding as of September 29, 2023.”

JPMorgan Chase’s 10-Q report for the quarter ending September 30 that it filed with the Securities and Exchange Commission indicated that it had $37.88 billion in outstanding advances from Federal Home Loan Banks as of the end of the third quarter. It reported that $26.2 billion of that was related to its acquisition of First Republic Bank. That would mean that the largest bank in the United States – which has the ability to borrow from the Federal Reserve’s Discount Window or the Fed’s $500 billion Standing Repo Facility – elected instead to tap almost $12 billion from a government mortgage program for low income families and not repay another $26 billion owed in relation to its acquisition of First Republic Bank.

JPMorgan Chase is an unreformed, serial recidivist bank that has admitted to five criminal felony counts brought by the U.S. Department of Justice since 2014. Just this year it has agreed to settle charges in two federal lawsuits for $365 million that credibly alleged the bank had actively participated in the late Jeffrey Epstein’s sex trafficking of minors. Throughout its crime spree, the chummy Board of Directors at the bank has voted to keep the same man at the helm of the bank, Jamie Dimon, Chairman and CEO.

JPMorgan Chase’s questionable use of advances from the Federal Home Loan Banks dates back to at least 2013. On September 18, 2013 we reported that the largest borrower from Federal Home Loan Banks was JPMorgan Chase, which had $61.840 billion in advances outstanding as of June 30, 2013.

We also reported that as of June 30, 2013, JPMorgan Chase wasn’t just borrowing from one Federal Home Loan Bank, it was borrowing from three separate ones. We found that it had grabbed 65.8 percent of all advances made at the time by the Federal Home Loan Bank of Cincinnati, which services Kentucky, Ohio and Tennessee.

In addition to being the largest borrower from the Federal Home Loan Banks as of the second quarter of 2013, JPMorgan was also being sued for fraud by the Federal Home Loan Bank of Pittsburgh. According to a 2013 financial filing, on September 23, 2009, the Federal Home Loan Bank of Pittsburgh had filed two complaints in state court for the recovery of the Bank’s losses relating to nine private label mortgage-backed securities (MBS) purchased from J.P. Morgan Securities, Inc. in an aggregate principal amount of approximately $1.68 billion. According to the filing, some claims had been dismissed but there remained claims against JPMorgan “for fraud, negligent misrepresentation and state and federal securities law claims….”

JPMorgan Chase ended up paying the staggering sum of $13 billion to settle charges with the Justice Department and other regulators for selling toxic mortgage products. Instead of promoting a financially stable housing market, Jamie Dimon’s bank was a major participant in causing the worst housing price collapse since the Great Depression.

Another finding from the FHFA report is that the Presidents and CEOs of the Federal Home Loan Banks – which are Government Sponsored Enterprises (GSEs) with a public mission – are being grossly overpaid. The FHFA said it plans “to recommend that Congress amend the Safety and Soundness Act to eliminate the restrictions on the Agency’s authority to prescribe levels or ranges for the compensation of executive officers of the FHLBanks.”

Read More @ WallStOnParade.com