by Wolf Richter, Wolf Street:

![]()

As we have found out in the recent episodes of the commercial real estate nightmare, with landlords stiffing their creditors by either walking away from properties or loans and letting lenders take the massive losses: Those lenders have turned out to be mostly investors in Commercial Mortgage-Backed Securities (CMBS), Collateralized Loan Obligations (CLOs), and mortgage-REITS, not banks. Banks are taking some hits too, but not like these investors. Which gave rise to the theory around here that banks securitized most of their riskiest and worst CRE loans and sloughed them off years ago to investors that were chasing yield.

TRUTH LIVES on at https://sgtreport.tv/

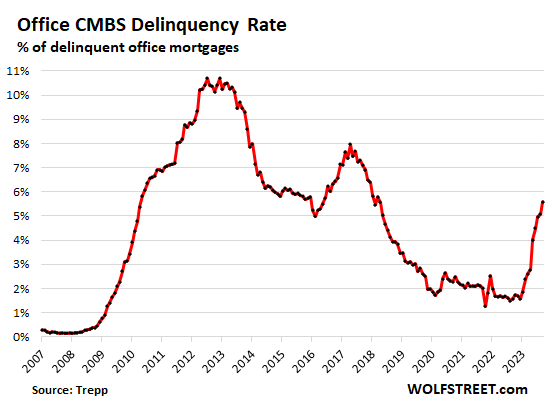

So the delinquency rate of commercial mortgages on office properties that had been securitized into CMBS spiked to 5.6% by loan balance in September, having more than tripled so far this year, from a delinquency rate of 1.6% in December, according to Trepp, which tracks and analyzes CMBS.

The cycle during the Financial Crisis, when delinquency rates eventually exceeded 10% in 2012 and 2013, started more slowly and proceeded more slowly than this cycle. This is a ferocious deterioration:

This time around, the landlords are walking away from the office properties or mortgages for two reasons:

- Huge vacancy rates that are now a structural problem as Corporate America has discovered that it doesn’t need and won’t ever need all this office space;

- CRE mortgage rates that have more than doubled, which is a killer when variable-rate mortgages aren’t sufficiently hedged, and it’s a killer when a maturing 3.5% fixed-rate mortgage needs to be refinanced with an 8% mortgage.

When this occurs, the interest expense that the landlord has to deal with can no longer be covered by rents, especially if the building has a low occupancy rate. And then it’s just a money pit. The landlord gives up the building, takes the loss on their equity, and lets these investors take the remaining losses.

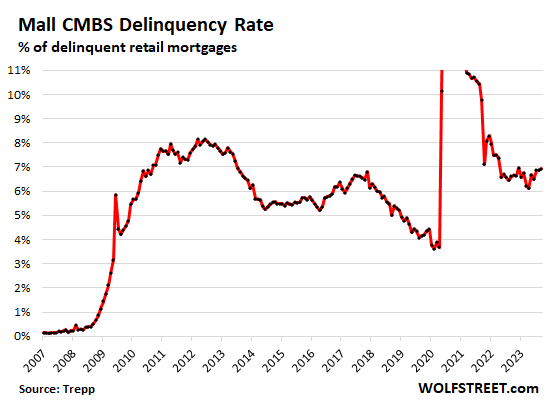

The fate is even worse for mall CMBS. Mortgages for malls have been in trouble for over a decade due to a structural shift to ecommerce that has killed innumerable malls – a process that I have called brick-and-mortar meltdown since 2016. It has caused landlords – even the biggest mall landlords, Simon Property Group and Brookfield – to walk away from mall after mall and let these investors take the losses. Zombie malls are everywhere. Eventually developers end up with them, bulldoze them, and build something else on that land, such as housing. And all along the way, CMBS investors have taken massive losses.

The delinquency rate of retail CMBS surged during the Financial Crisis. In the years after the Financial Crisis, as these loans were either taken out of the index after foreclosure or as the delinquency was cured, the default rate declined to just under a still high 4%, when the pandemic hit, and delinquencies spiked.

In September, the delinquency rate ticked up to 6.92%:

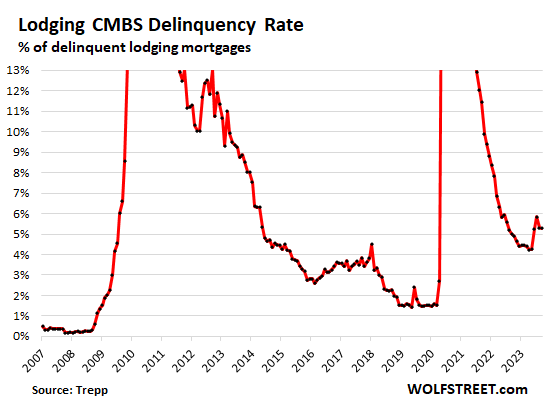

Lodging CMBS delinquency rates exploded during the Financial Crisis and during the pandemic, but then recovered, sort of. Lodging delinquencies remained high in September at 5.3%, roughly unchanged from August, but down from July (5.9%), and over three times the rate in 2019:

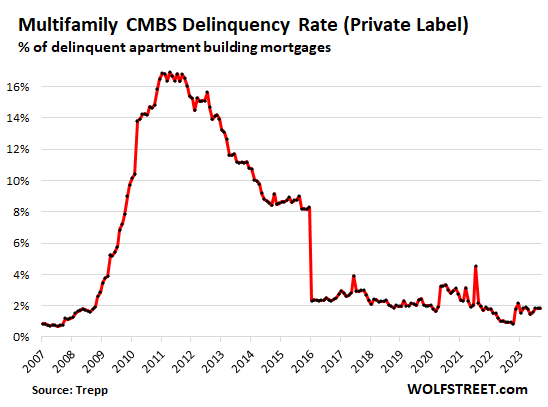

Multifamily delinquencies have been bobbing along relatively low levels still. In September, they ticked up to 1.85%. These are “private label” CMBS, not multifamily mortgages backed by the government.

There have been some big delinquencies, including the mortgages backed by a portfolio of 75 apartment buildings owned by Veritas in San Francisco, which caused the delinquency rate to jump in December 2022.

There is demand for apartments, unlike offices, and it’s not a problem of not being able to find tenants. The problem with some of these mortgages is the interest cost. When the mortgage comes due and has to be refinanced with a much higher rate, or if it’s a variable-rate mortgage, then the difficulties arise.

In the chart below, the plunge in the delinquency rate in January 2016 occurred because a huge delinquent loan was resolved, backed by Stuyvesant Town–Peter Cooper Village, a residential development in Manhattan with 110 apartment buildings. Blackstone and Ivanhoe Cambridge agreed to pay $5.3 billion in 2015 for the 80-acre property. After the deal closed in December 2015, the $3 billion in CMBS loans tied to the property was paid off, triggering the drop in the CMBS delinquency rate in January 2016.

Industrial delinquencies remain low. These loans are backed by warehouses and fulfillment centers, and they have been in high demand due to the boom in ecommerce. Demand has softened a little, as Amazon walked back some of its massive expansion plans. But in September, delinquency rates remained at 0.3%, the envy of the other major categories: