by Pam Martens and Russ Martens, Wall St On Parade:

On May 1, the Federal Deposit Insurance Corporation announced that First Republic Bank had failed and that it was being sold to JPMorgan Chase. At the time, JPMorgan Chase was already the largest and riskiest bank in the United States. The sweetheart deal the bank got from the FDIC to take over First Republic included the FDIC eating 80 percent of any losses on single-family residential mortgages for 7 years and 80 percent of any losses on commercial loans, including commercial real estate, for five years. The FDIC also provided JPMorgan Chase with a $50 billion, five-year fixed-rate loan at an undisclosed interest rate.

On May 1, the Federal Deposit Insurance Corporation announced that First Republic Bank had failed and that it was being sold to JPMorgan Chase. At the time, JPMorgan Chase was already the largest and riskiest bank in the United States. The sweetheart deal the bank got from the FDIC to take over First Republic included the FDIC eating 80 percent of any losses on single-family residential mortgages for 7 years and 80 percent of any losses on commercial loans, including commercial real estate, for five years. The FDIC also provided JPMorgan Chase with a $50 billion, five-year fixed-rate loan at an undisclosed interest rate.

TRUTH LIVES on at https://sgtreport.tv/

According to the filing that JPMorgan Chase made with the Securities and Exchange Commission last Friday, the deal also gave JPMorgan Chase something that it desperately needed: deposits. According to the 8-K filing that JPMorgan Chase made with the SEC on October 13, the acquisition of First Republic Bank added $47.2 billion to its deposit base in the second quarter and $66.7 billion in deposits in the third quarter.

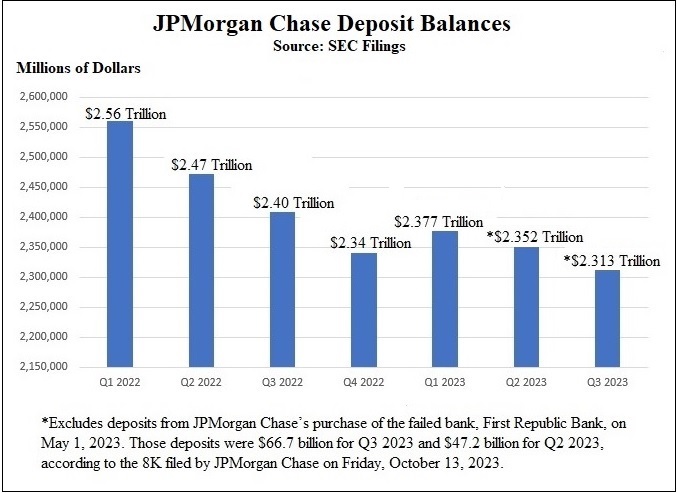

As the chart above indicates, JPMorgan Chase suffered outflows of deposits in every quarter of 2022. It got a brief respite from inflows of deposits in the first quarter of 2023, as a result of the March banking panic that impacted smaller banks, then outflows took hold again. Excluding the deposits from First Republic Bank, JPMorgan Chase has lost $248.38 billion in deposits over the span of the last seven quarters. One doesn’t expect that at a bank that continues to trumpet its “fortress balance sheet.”

Even including the large amount of deposits that JPMorgan Chase gained from scooping up First Republic, the bank still bled $19.4 billion in overall deposits between the second quarter of this year and the end of the third quarter on September 30, according to JPMorgan Chase’s SEC filing on Friday, October 13.

Adding to the appearance of desperation at JPMorgan Chase to shore up its deposit base, on September 28 Wall Street Journal reporter Rachel Louise Ensign revealed that JPMorgan Chase was offering a shockingly high 6 percent interest on a 6-month certificate of deposit. There were three catches to get the deal: it had to be new money coming from outside the bank; the minimum investment was $5 million; and the money had to be deposited by September 30. The date of September 30 just happens to be the last day of the quarter, the cutoff for the bank to report its final tally for deposits at quarter end.

There is something else remarkable about that uncharacteristic spurt of generosity from JPMorgan Chase. By soliciting a minimum of $5 million in new outside money to get the 6 percent CD, the bank would appear to be effectively soliciting to grow its already eyebrow-raising amount of uninsured deposits. The FDIC insures deposits up to $250,000 per depositor, per bank. The Wall Street Journal article is silent on how the balance of the $5 million would be protected.

According to the bank’s regulatory filings, as of December 31, 2022, JPMorgan Chase Bank N.A. held $2.015 trillion in deposits in domestic offices, of which $1.058 trillion were uninsured. The bank also held another $418.9 billion in deposits in foreign offices, which were also not insured by the Federal Deposit Insurance Corporation (FDIC). That brought its uninsured deposits as of year-end to a total of $1.48 trillion or 60 percent of its total deposits. (Under federal statute, the deposits held by U.S. banks that are located on foreign soil are not insured by the FDIC. )

After the second, third and fourth largest bank failures in U.S. history over the span of seven weeks this past spring, the FDIC has awakened to the dangers of U.S. banks holding large amounts of uninsured deposits – whether they are uninsured because they exceed the $250,000 insurance cap per depositor/per bank or are uninsured because the deposits reside on foreign soil. Large holdings of uninsured deposits contributed to the bank runs at Silicon Valley Bank and Signature Bank in March, which toppled the banks and forced an FDIC receivership at both banks until they were eventually sold. (First Republic Bank also had a large amount of uninsured deposits.)

Because billions of dollars in domestic uninsured deposits were at risk at the two banks that failed in March, federal regulators issued a “special risk assessment” that allowed the FDIC to cover all uninsured domestic deposits at those two banks. That action resulted in billions of dollars in extra losses to the FDIC’s Deposit Insurance Fund (DIF).

Read More @ WallStOnParade.com