by Pam Martens and Russ Martens, Wall St On Parade:

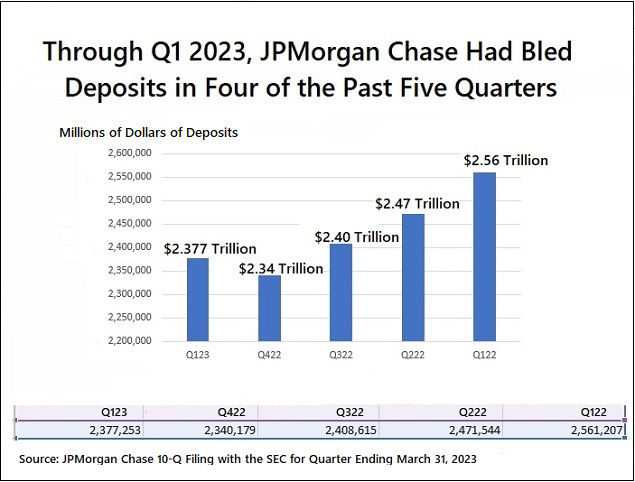

The data in the chart above comes directly from what the biggest bank in the United States, JPMorgan Chase, reported on its 10-Q filing with the Securities and Exchange Commission (SEC) for the quarter ending March 31, 2023. Despite all those mainstream media headlines and news stories about the biggest banks in the U.S. being the deposit beneficiaries of the banking panic earlier this year, the cold, hard facts on the ground are the following: at the end of the first quarter of this year, JPMorgan Chase had seen deposit outflows in four out of the past five quarters. Mainstream media conveniently forgot to mention that.

TRUTH LIVES on at https://sgtreport.tv/

The only quarter in which JPMorgan Chase saw an inflow of deposits was the first quarter of this year, when three banks blew up: Silvergate Bank, Silicon Valley Bank and Signature Bank. That increase was a mere pittance compared to the huge outflows of deposits it had already suffered in 2022.

Now we are getting an even clearer picture of the downward trend in deposits at JPMorgan Chase thanks to the 8-K filing that the bank made with the SEC on July 14. Had it not been for that sweetheart deal that the FDIC cooked up with JPMorgan Chase in the second quarter of this year, allowing it to buy the good stuff it wanted from the failed First Republic Bank, while regulators ate the bulk of the bad stuff, JPMorgan Chase would have had another decline in deposits in the second quarter.

According to the 8-K filing, First Republic added $68.351 billion to JPMorgan’s deposits for the period ending June 30, 2023. Without those deposits, JPMorgan Chase’s deposits would have stood at $2.33 trillion as of June 30, representing a quarter-over-quarter decline in deposits of $46.64 billion. That would have brought the outflow of deposits since the end of the first quarter of 2022 to a whopping $230.6 billion, and showing that the bank lost deposits in five of the last six quarters.

The bank’s so-called fortress balance sheet is starting to look like there are termites gnawing at the timbers. (See also: JPMorgan Chase Transferred $347 Billion in Debt Securities Over the Last 3 Years to Inflate Its Capital Using a Controversial Maneuver.)

JPMorgan Chase getting the greenlight from federal regulators to purchase the failed First Republic Bank was a demonstration of regulatory capture at its worst. Despite JPMorgan Chase having admitted to five felony counts brought by the U.S. Department of Justice since 2014; despite it having an organized crime style rap sheet; and despite it being currently scandalized around the globe for functioning as the cash conduit for Jeffrey Epstein’s sex-trafficking of school-age girls for more than a decade, this is the sweetheart deal the bank got from the FDIC to take over First Republic: the FDIC would eat 80 percent of any losses on single-family residential mortgages for 7 years and 80 percent of any losses on commercial loans, including commercial real estate, for five years. The FDIC also provided JPMorgan Chase with a $50 billion, five-year fixed-rate loan at an undisclosed interest rate.

Read More @ WallStOnParade.com