by Alasdair Macleod, GoldMoney:

Silver prices have strengthened remarkably over the past few months. In the fall of 2022, the metal had dropped to around $18/ozt, the lowest since early 2020. Since then, silver has pushed higher and is now again hovering around $25/ozt. The recent strength in silver prices comes on the back of stronger gold prices. Gold once again is trading at over $2000/ozt, close to its all-time high.

A few years ago we introduced our silver price model to our readers (Silver price framework: Both money and a commodity, March 9, 2017). In that report we presented the following findings:

TRUTH LIVES on at https://sgtreport.tv/

While market analysts, financial media, and commodity investors often regard silver as gold’s temperamental cousin, simply viewing silver as a more volatile version of gold fails to give the metal due consideration. Just as the physical properties of gold destined it to become an ideal store of value, silver’s properties make the metal special in its own right.

As explained in our Gold Price Framework, gold is not a flow commodity. Historical currency correlations and rate-driven volatility indicate that gold trades as a money stock; however, silver is special because it’s similarly well-suited to be money as well as an input commodity consumed in a variety of industrial processes.

Thus, silver prices are driven by monetary demand as well as supply and demand for industrial purposes, the latter of which is an important differentiator. Above ground gold stocks have always grown at the same pace as new gold is mined, dampening the effects of inventory-determined price volatility; however, silver stocks grew much more slowly as industrial demand absorbed a large part of what is mined.

1. Silver is, like gold, a commodity store of value and free of counterparty risk, with energy-intensive replacement costs setting the lower boundary for prices (the same energy proof of value that underlies gold prices). As such, silver should be impacted by the same monetary drivers as gold prices: real-interest rate expectations, central bank policy, and longer-dated energy prices.

2. As silver is a commodity with extensive industrial applications, changes in industrial drivers (i.e. changes in available inventories) should impact the price of the metal.

This means that there is a strong relationship between silver prices and the level of economic activity on top of the impact that stems from the monetary environment. Hence, from that perspective, silver should underperform gold in a recession. As we believe that a recession is rather imminent – we have highlighted this in some of our reports over the past weeks – what does that mean for silver prices?

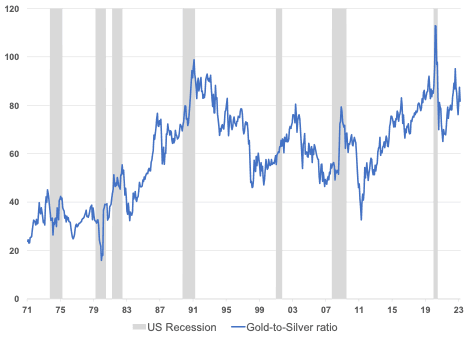

When we look at the historical ratio between gold and silver, it is indeed true that during the last five recessions, the gold-to-silver ratio (GTS-ratio) increased (see Exhibit 1). In three of those five instances we saw a very sharp upward move:

Exhibit 1: Gold outperformed silver over the last five recessions

Source: Goldmoney Research

2020 COVID19 pandemic: Most governments opted for a similar response to the COVID19 pandemic by locking down large parts of their respective countries for weeks, in some instances months. This led to a sharp contraction in economic activity in 1H2020. During the initial phase of this rather unique recession, the GTS-ratio jumped from 85 to 112. This came mainly on the back of a sharp decline in silver prices from $18/ozt to $12/ozt, while gold prices increased only slightly from $1600/ozt to $1700/ozt.

2008 Great Financial Crisis: The GFC triggered a global recession that lasted two years from 4Q2007 to 3Q2009. During that time, the GTS-ratio went from 54 to 68. However, the GTS-ratio jumped as high as 80 in late 2008 at the peak of the panic in financial markets. While the move higher in the ratio was mainly due to the increase in gold prices, the peak in the ratio in late 2008 came on the back of a collapse in silver prices from $15/ozt prior to the recession to under $10/ozt.

The 2001 Dot.Com crash: The bursting of the Dot.com bubble lead to a recession that lasted from 1Q2001 to 3Q2001. During that time, the GTS-ratio moved only marginally higher from 55 to 63. This was mainly due to slightly higher gold prices while silver prices moved marginally lower. At the end of the recession, gold was trading at $290/ozt and silver at $4.50/ozt

The early 1990s recession: The recession in the early 1990s lasted from 4Q1989 to 1Q1991 in the US. During that time, the GTS-ratio shot up from 69 to 98. Gold prices remained more or less stable over the entire timeframe while silver prices declined from $5.30/ozt to $3.80/ozt.

The Recession of 1981–82: The recession of 1981 was the result of tight monetary policy by the Fed (and other central banks) in an effort to fight mounting inflation. The late 1970s early 1980s were plagued by double digit inflation. Fed chairman Volker drastically raised interest rates to over 20% which eventually brought inflation under control, but also triggered another recession. During the 1981-1982 recession, the GTS-ratio went from 41 to 55. Both gold and silver prices declined sharply during that period, but silver more. Gold went from $500/ozt to $300ozt and silver from $12.30/ozt to $5.30/ozt. It is important to highlight that these price corrections came after a decade of relentless rallies in metal prices on the back of high inflation (see Exhibit 2).

Exhibit 2: The decline in precious metal prices during the 1981-1982 recession followed more than a decade of rising prices on the back of relentless inflation