by Pam Martens and Russ Martens, Wall St On Parade:

On April 11, Wall Street On Parade ran this headline: Fed Report: Largest 25 U.S. Banks Have Shed $700 Billion in Deposits Over Past Year. Using deposit data directly from the Federal Reserve’s weekly H.8 report, we documented that contrary to the misleading reporting in the mainstream business press, it wasn’t the regional banks that were losing the bulk of deposits in the U.S., with the biggest banks the beneficiaries, it was actually the biggest banks that were dramatically shedding deposits. We explained as follows:

TRUTH LIVES on at https://sgtreport.tv/

“The reality is that the 25 largest domestically-chartered commercial banks in the U.S. have been bleeding deposits for most of the past 12 months, shedding more than $700 billion in deposits between April 13, 2022 and March 29, 2023. To put that in even sharper focus, all U.S. domestically-chartered commercial banks have lost a total of $970 billion during the same time period. That means that the largest 25 banks account for a whopping 72 percent of the plunge in deposits over the past year.”

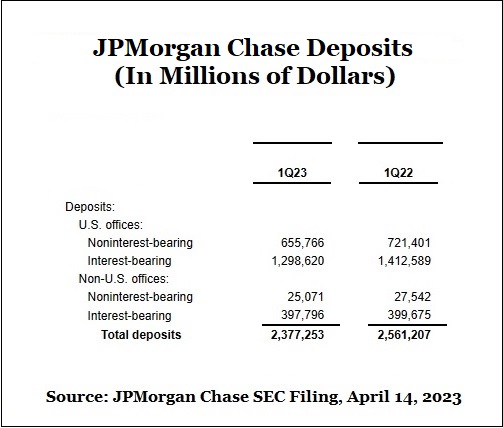

On Friday, we learned more granular details about this deposit exodus when JPMorgan Chase and Citigroup announced first quarter earnings and released data on their deposits. According to its own figures, JPMorgan Chase experienced an outflow of $183.95 billion in deposits between March 31, 2022 and March 31, 2023. In dollar terms over that time span, its deposits went from $2.561 trillion to $2.377 trillion. (See chart below.)

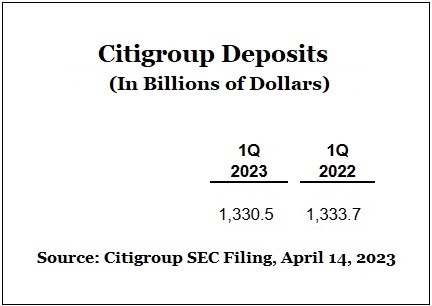

Making that news even more astonishing (given all the media reports that suggested JPMorgan Chase would be a beneficiary of the exodus of deposits from troubled regional banks), was that a peer bank holding company, Citigroup – parent of the commercial bank, Citibank – reported a decline in deposits over the same period of just $3.2 billion.

How is it possible that Jane Fraser, CEO of Citigroup, was able to hold onto her deposit base while Jamie Dimon, Chairman and CEO of JPMorgan Chase (who incessantly brags about his “fortress balance sheet”) experienced a depositor revolt that was 57 times that of Citigroup?

In the earnings call with analysts on Friday, Fraser had this to say:

“Indeed, the cornerstone is our institutional deposit base, which comprises about 60 percent of our deposits. Most of these deposits are particularly sticky because they sit in operating accounts that are fully integrated into how our multinational clients run their businesses around the world from their payrolls, their supply chains, their cash and liquidity management.

“Eighty percent of these deposits are with clients who use all three of our integrated services: payments and collections, liquidity management and working capital solutions. The data that we aggregate from these deposits and their related flows is fundamental to how our clients manage their efficiency, risk and compliance. And this greatly increases our deposit stickiness. It’s also why nearly 80 percent of these deposits are from client relationships that are 15 years old or more.”

The fact that 80 percent of Citi’s deposit relationships are at least 15 years old means that these clients remember what happened in 2008 when Citigroup was teetering on the brink of failure. In fact, Citigroup’s share price of 99 cents in early 2009 makes some troubled regional banks today look positively healthy.

Read More @ WallStOnParade.com