by Peter Schiff, Schiff Gold:

Similar to last month, the Treasury is using extraordinary measures to keep the total debt balance below the current debt ceiling.

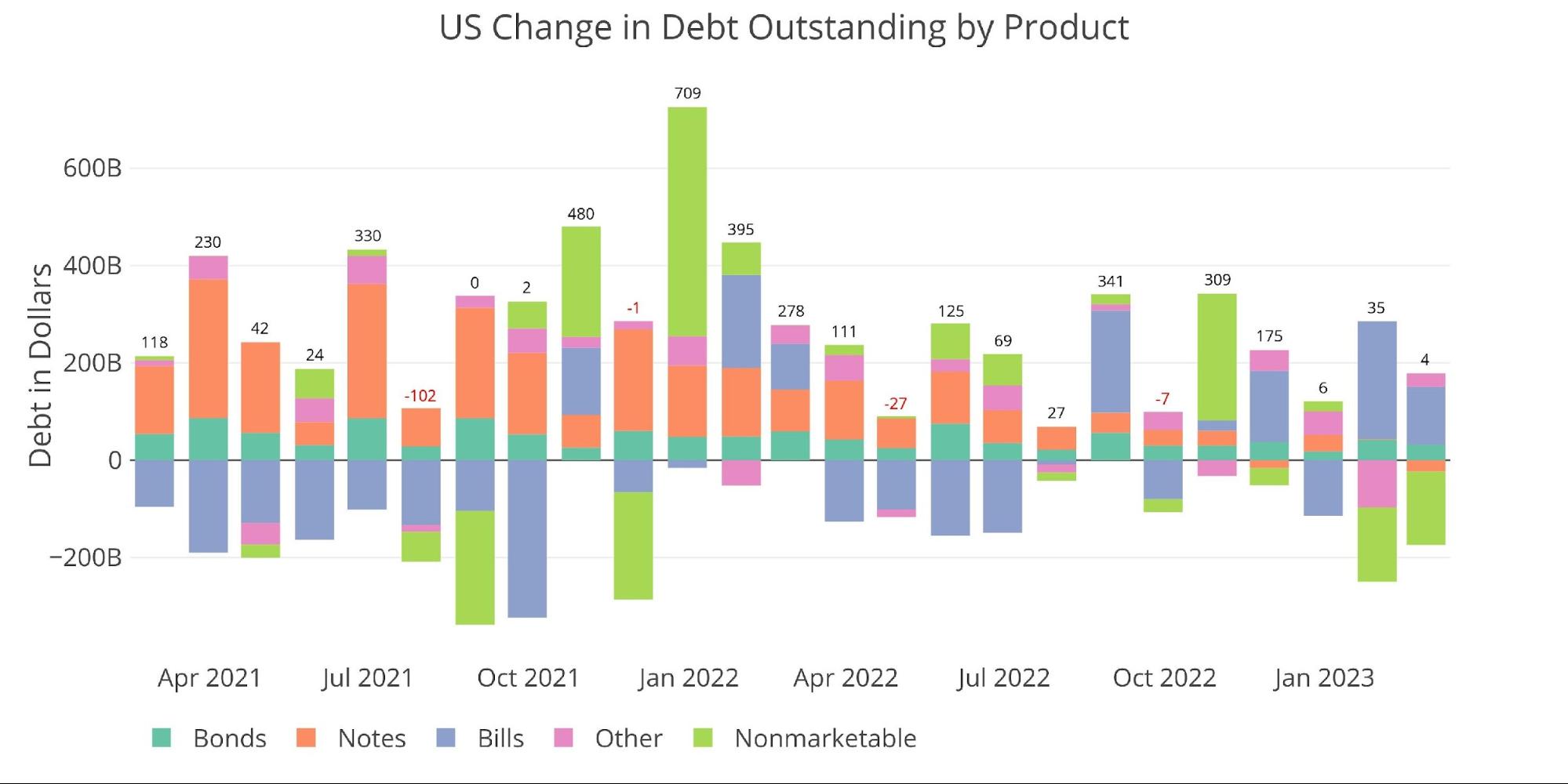

The big moves this month were rolling off $150B in Non-Marketable security to allow $120B in T-Bills to be added to the debt. With all the moves, the total effect on the debt was to add only $4B.

Note: Non-Marketable consists almost entirely of debt the government owes to itself (e.g., debt owed to Social Security or public retirement)

TRUTH LIVES on at https://sgtreport.tv/

Figure: 1 Month Over Month change in Debt

Given the current debt ceiling saga, the total debt added for the current calendar year does not amount to anything material. The only thing to really notice is the big surge in short-term debt issuance. The Treasury is using short-term bills because they will be easier to roll off once the debt ceiling saga ends and replace with non-Marketable debt.

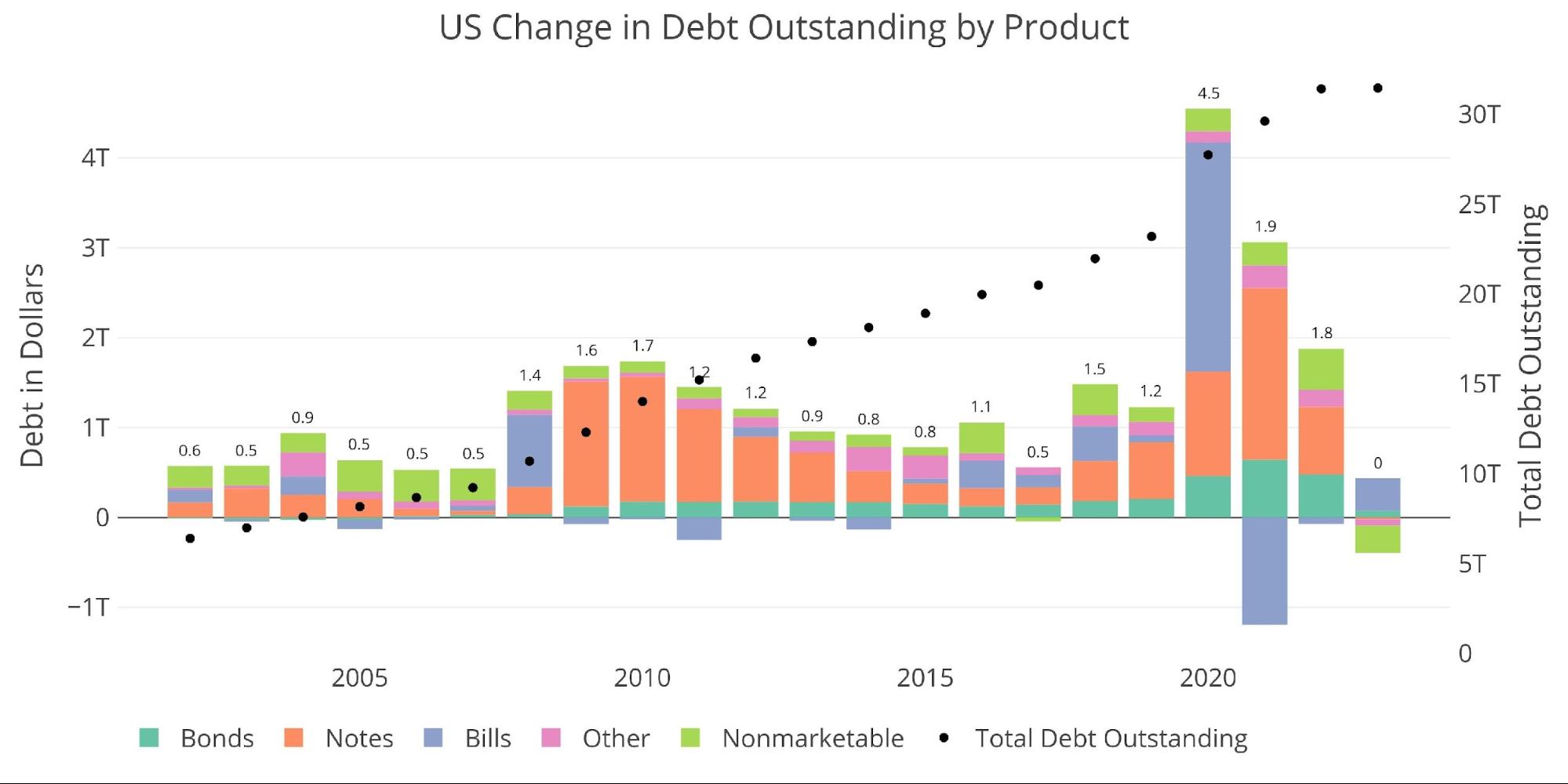

Figure: 2 Year Over Year change in Debt

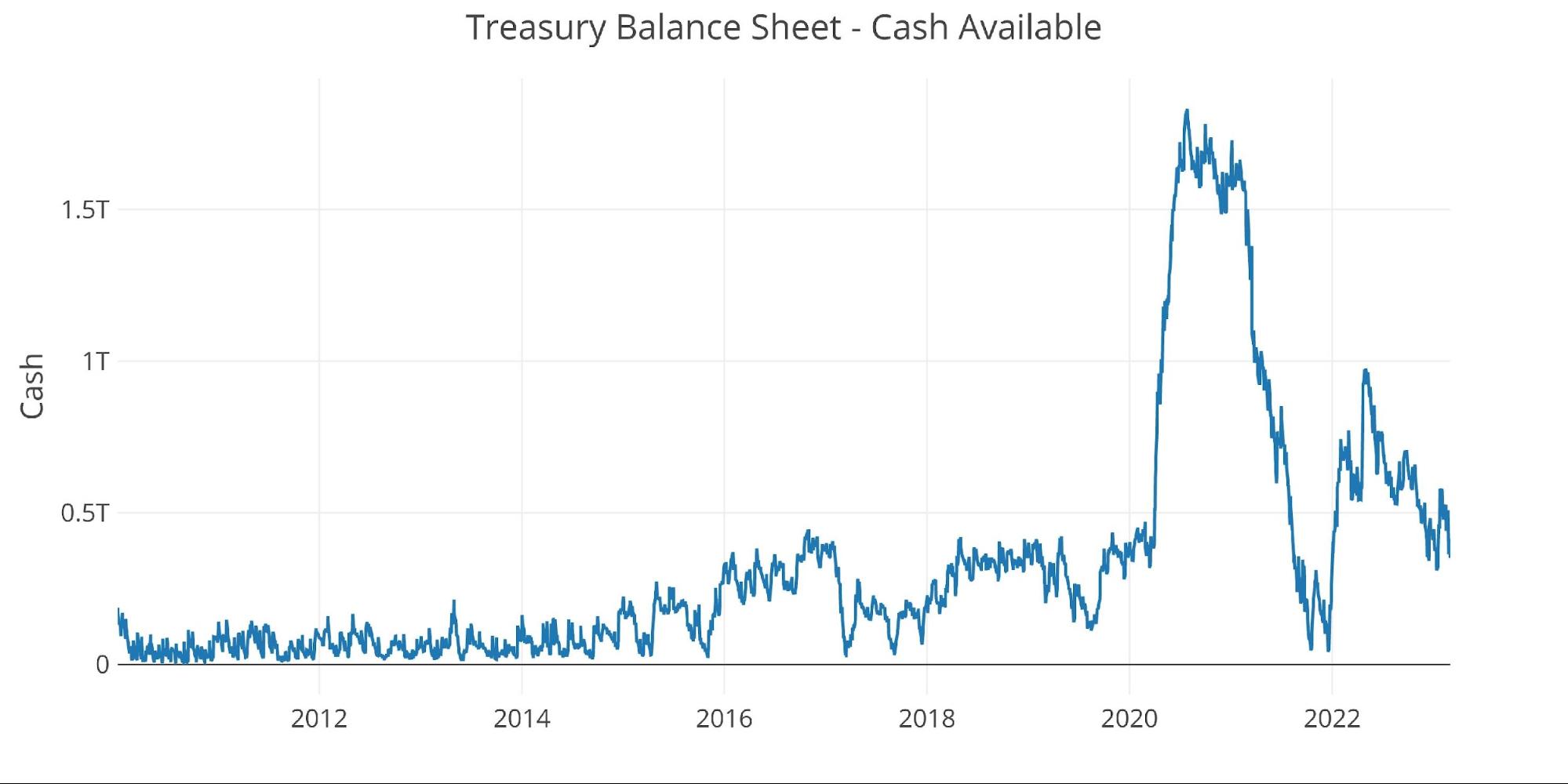

In addition to using extraordinary measures with Non-Marketable debt, the Treasury has additional room to maneuver with the cash balance it holds currently. It currently sits at $351B, but that is down from $580B as recently as January.

Figure: 3 Treasury Cash Balance

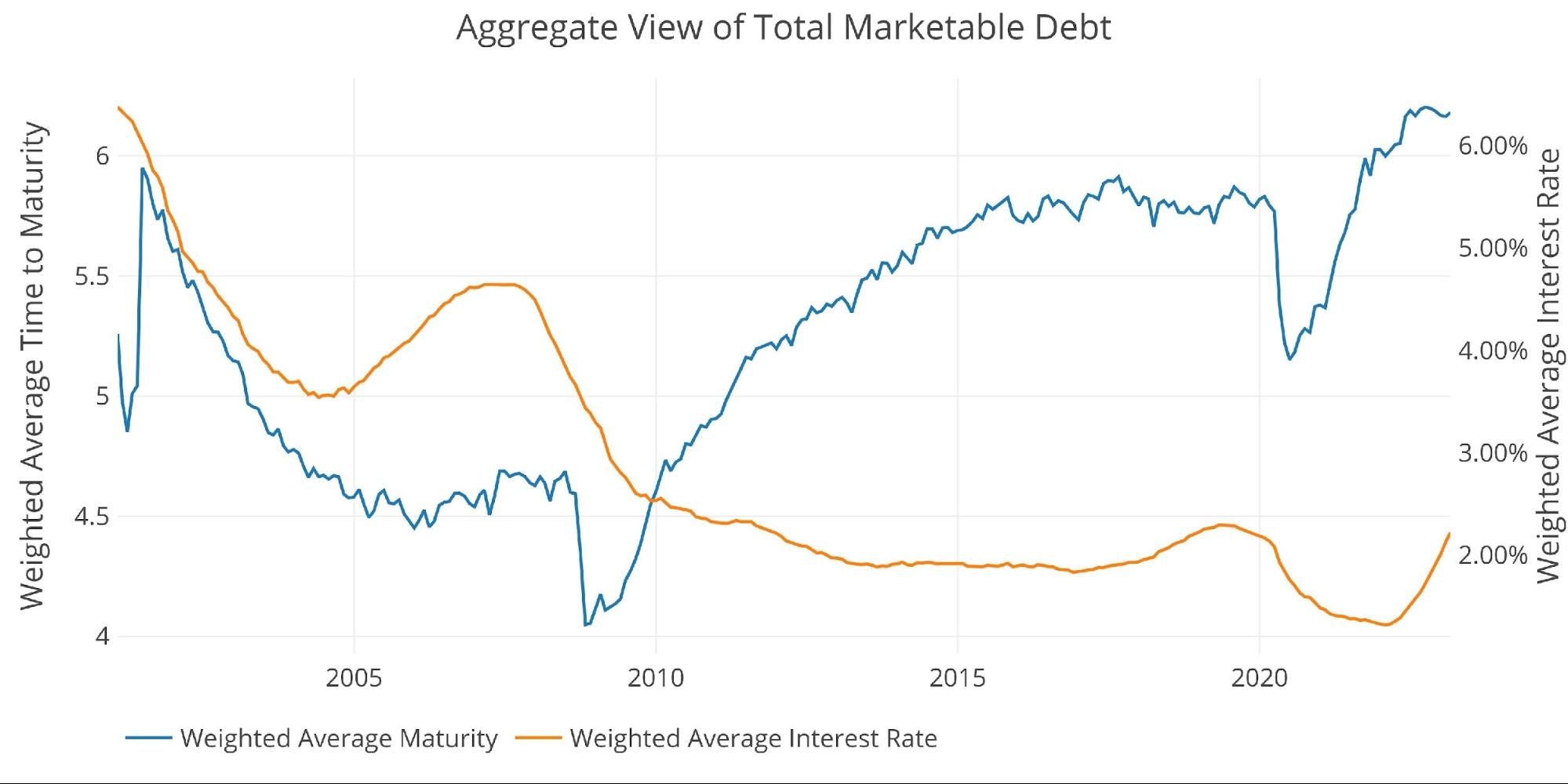

Average maturity on the debt has mostly stabilized in recent months, but the weighted average interest rate continues to rise precipitously. It now stands at 2.22%, up from 1.32% only one year ago.

Figure: 4 Weighted Averages

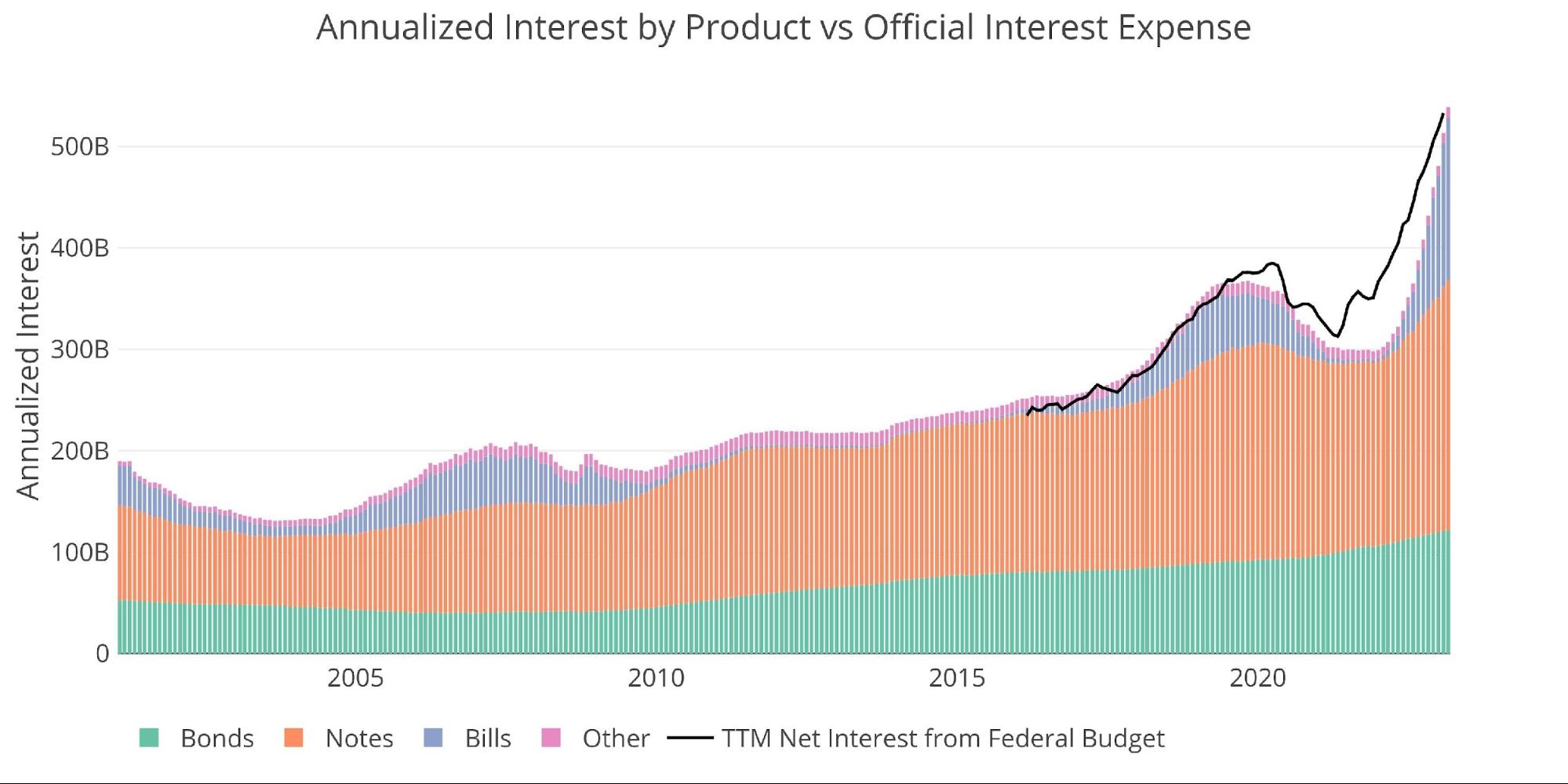

The impact of rising rates can be seen below, specifically the blue bars which represent short-term Bills. Interest is exploding upwards at an unsustainable pace. Annualized interest on the debt increased by $25B in a single month. This means that in 30 days, the cost of servicing the debt annually increased by almost 5%. That is an incredible rate of increase!

In a single year, debt servicing costs have risen an incredible 75%.

Figure: 5 Net Interest Expense

More concerning is the trajectory of the move. Even though the Fed is getting ready to slow the pace of interest rate hikes, it does not mean that debt servicing costs are set to slow. As the chart below shows, more debt will be rolling over at the higher rates.

As shown above in Figure 3, the average weighted interest rate is 2.22%. The entire yield curve is near or above 4%. As debt rolls over and new debt is issued, interest costs continue to rise even if the Fed doesn’t hike rates anymore. Based on the current trajectory, by this time next year, debt interest costs could exceed $750B!