by Wolf Richter, Wolf Street:

![]() Mostly taxpayers, not the banks.

Mostly taxpayers, not the banks.

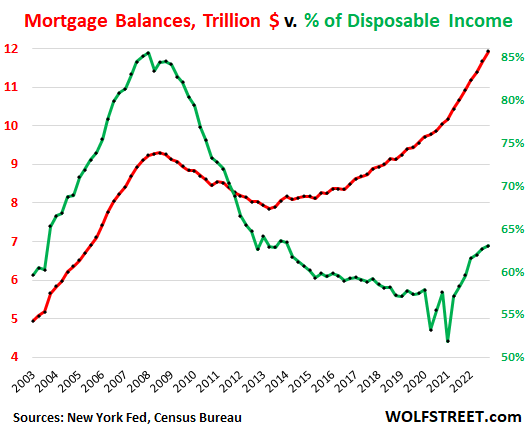

Mortgage balances ballooned because home prices ballooned in recent years, requiring more debt to finance the same home, and so mortgage balances in Q4 rose 2.2%, or by $253 billion, from the prior quarter, and by 9%, or by $1 trillion, from a year earlier, even as home sales volume plunged by 34% in Q4. Mortgage balances now reached $11.9 trillion.

TRUTH LIVES on at https://sgtreport.tv/

Over the three-year period that covers the Fed’s pandemic-era money-printing binge and interest-rate repression, mortgage balances exploded by 25%, according to the New York Fed’s data on household credit. Over the same period, the median home price ballooned by 34%, according to the National Association of Realtors, even after the 11% drop from the peak in June 2022.

The chart also shows mortgage debt as a percent of disposable income (green), a measure of the aggregate burden of this mortgage debt on households. It shows why the Housing Bust in 2005-2012 was such a mess, and it also shows one of the reasons the same kind of mortgage crisis is now unlikely. But the home-price inflation since 2020 has started leaving its mark on the ratio – after the pandemic monies stopped inflating disposable income:

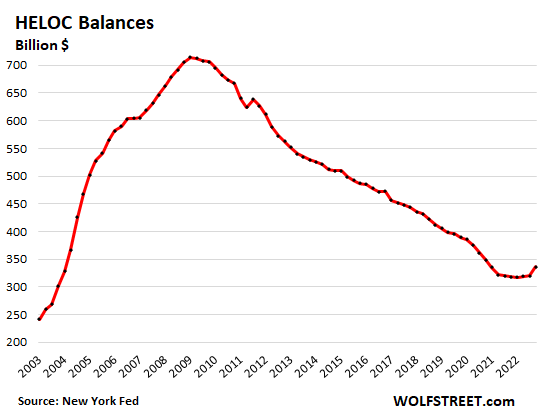

HELOCs are one of the classic ways to use home equity as an ATM. But cash-out refis at ultra-low interest rates nearly killed the HELOC business. And now it’s coming back in baby steps.

HELOC balances, after creeping along at very low levels since early 2021, rose by 5.0% in Q4 from Q3, or by $16 billion, to $340 billion.

Mortgage and HELOC delinquencies have inched up from historic lows but remain very low.

For mortgages, the 30-day-plus delinquency rate – the rate of borrowers who newly transition into delinquency – ticked up for the third month in a row to 2.3% (red line in the chart below), which was still below any pre-pandemic low in the data going back to 2003.

During the Good Times before Housing Bust 1, in 2005, the delinquency rate bottomed out at 4.6%. During the Good Times before the pandemic, the delinquency rate bottomed out at 3.4%.

The 30-plus-days delinquency rate of HELOCs ticked down for the second month in a row, to 2.0%, right in line with the Good Times: