by Michael Snyder, The Economic Collapse Blog:

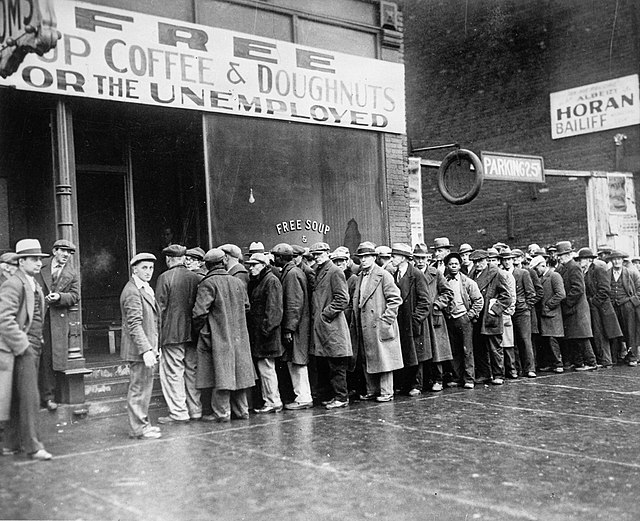

Economic conditions are much worse than you are being told. Throughout the past year, prices have been rising much faster than most of our incomes have. As a result, our standard of living has been rapidly declining. It has become increasingly difficult for U.S. households to make it from month to month, and as you will see below, more than a third of all U.S. adults are actually relying on their parents to pay at least some of their bills at this point. But even more alarming is what has been happening to real disposable income. According to Fox Business, the most recent GDP report revealed that the decline in real disposable income that we witnessed in 2022 was the largest that has been measured since 1932…

TRUTH LIVES on at https://sgtreport.tv/

The most troubling information in the GDP report is the precipitous drop in real disposable income, which fell over $1 trillion in 2022. For context, this is the second-largest percentage drop in real disposable income ever, behind only 1932, the worst year of the Great Depression.

Just think about that for a moment.

The last time real disposable income declined this quickly was literally during the peak of the Great Depression.

And as our incomes get squeezed tighter and tighter, more Americans are starting to fall behind on their bills.

For example, the proportion of subprime auto borrowers that are at least 60 days behind on their payments has just surged to the highest level that we have seen since 2008…

In December, the percentage of subprime auto borrowers who were at least 60 days late on their bills climbed to 5.67% — a major increase from a seven-year low of 2.58% in April 2021, according to Fitch Ratings. It marks the steepest rate of Americans struggling to make their car payments since the 2008 financial crisis.

We are already beginning to witness the largest tsunami of repossessions that we have seen since the “Great Recession”, and it is only going to get worse in the months ahead.

One woman in San Antonio that knows that her vehicle could be repossessed at any time has decided that hiding it is the best strategy for now…

For some, however, the only lesson is to try and outsmart the repo man: hardly the best long-term strategy. Take San Antonio native Zhea Zarecor who is currently trying to negotiate with her lender so her 2013 Honda Fit won’t get repossessed. In the meantime, she’s hiding it.

The 53-year-old, who is currently in school for her bachelor’s in information technology (and raking up massive student loans for an education she should have had some 35 years ago) splits the monthly bill for the car — about $178 — with her roommate. But then the roommate lost his job, and with prices for groceries and everyday items increasing, there just wasn’t enough for the car payments.

Zarecor is trying to make extra money with odd jobs like contract secretarial work and participation in medical studies, but it often feels hopeless, she said. “Our money doesn’t go as far as it used to,” she said. “I don’t see prices going down, so the only relief I see is when I get my degree.”

Sadly, most of the country is just barely scraping by at this juncture.

As I discussed in a previous article, one recent survey discovered that 57 percent of Americans cannot even afford to pay a $1,000 emergency expense right now.

And a different survey has found that a whopping 35 percent of all U.S. adults are still relying on Mom and Dad to pay at least some of the bills…

More than one third of adults (35%) admit they still have at least one bill on their parents’ tab. According to a new poll of 2,000 Americans, the top three expenses their parents still pay for are rent (19%), groceries (19%), and utilities (16%). In fact, almost one-quarter (24%) of millennials say their parents cover their rent.

Are things really this bad?

Unfortunately, economic conditions are only going to get even worse in the months ahead as countless more Americans lose their jobs.

On Monday, I was quite saddened to learn that electronics giant Philips will be giving the axe to another 6,000 workers…

Philips announced Monday that it’s cutting another 6,000 jobs worldwide as it works to boost profitability.

The workforce reduction will occur over the next two years with the first 3,000 cuts taking place this year, the Dutch consumer electronics and medical equipment maker said on Monday. In its earnings report, the company revealed it suffered a net loss of 1.6 billion euros in 2022, which is down from a net profit of 3.3 billion euros last year.

And it is also being reported that one of my favorite toymakers has decided to eliminate approximately “15% of its global full-time workforce”.

I could go on and on if you would like.

In fact, every day I could fill up my articles with nothing but job loss announcements.

We have entered a very painful economic downturn, and one prominent Wall Street economist is warning that the full impact of this crisis will not be felt until the second half of 2023…

According to one Wall Street economist, a looming recession this year will feel more like the 1970s than a 2008-07 slump.

“People are too focused on ‘08 and 2020. This is more like 1973, 74 and 2021,” Piper Sandler chief global economist Nancy Lazar said on “Mornings with Maria” Monday.

Lazar predicted feeling the full impact of a recession in the second half of 2023 as lag effects from the Federal Reserve’s rate hikes take hold.

Actually, it would be quite wonderful if her seemingly gloomy forecast is accurate.

Because I don’t believe that we are heading into a slowdown like we experienced during the early 1970s.

Rather, I see all sorts of evidence that indicates that we are in the very early stages of the economic equivalent of “the Big One”.

Read More @ TheEconomicCollapseBlog.com