by Claudio Grass, Claudio Grass:

What physical precious metals investors can expect 2023 and beyond

Throughout the better part of 2022 there has been one question that has consistently, and predictably, popped up in conversations with my friends, clients and readers. Those who know me and are familiar with my ideas are well aware of my position on precious metals and the multiple roles they serve, so I can’t blame them for them for being curious whether I still “stick to my guns” in this era of irrationality in the markets and the economy. Especially for those not versed in monetary history, which is regrettably the vast majority of the population, it is natural to wonder: “If gold is such a great hedge against inflation, why hasn’t it skyrocketed now that inflation is finally here?”.

TRUTH LIVES on at https://sgtreport.tv/

Well, there are a couple of reasons for that, some more obvious than others. The interest rate hikes that the Fed spearheaded and repeatedly escalated are the most straightforward explanation. At least that’s the answer most mainstream economists and analysts will give you. And it makes sense: If gold pays you no interest for holding it, then why not switch to something that does? This is the mindset of most investors and that weakens demand, which in turn drags the price down. That’s how the theory goes anyway.

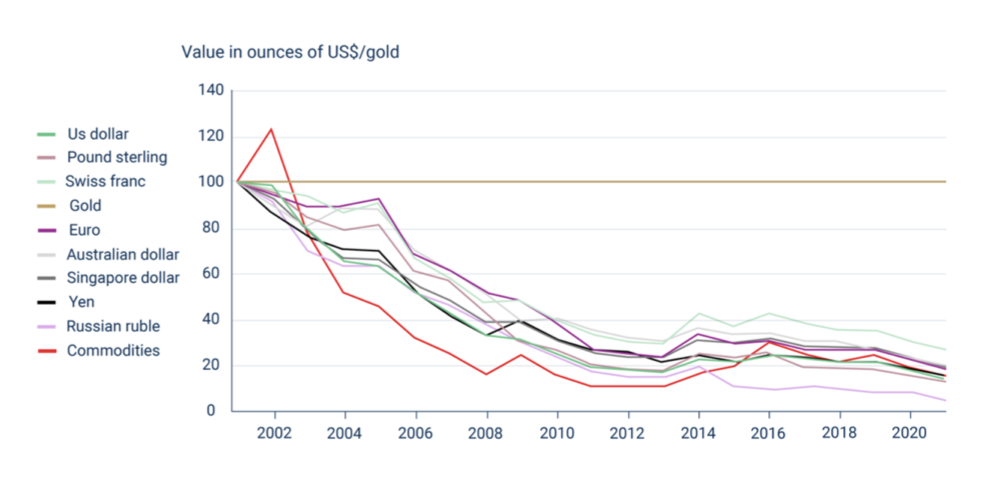

If, however, we’re willing to examine the question a little more closely, we might begin by scrutinizing its premises. The question takes for granted that gold has underperformed this year. But has it really? If you’re saving, getting your paycheck and paying your bills in a currency other than the dollar, you’re likely to have a very different view on this issue. In euros, gold is up around 6.6%. In yen, it’s up 17.9% In Egyptian pounds is up over 45%. What this clearly shows us, is that perspective matters.

And for those that can see the bigger picture, that perspective is even clearer: Thinking about the gold price in terms of any fiat currency, not just the USD, is not really helpful. It’s not gold’s value that fluctuates, what fluctuates is the perceived and totally imaginary value of all these useless pieces of paper. After all, as all long-term, responsible precious metals investors know very well, there’s only one important trend and its an obvious one, as the chart below shows.

As I mentioned many times, I do not believe that short-term price considerations should play a pivotal role in the decision making process of investors who hold gold for the right reasons and who understand why they do. What is important, however, is to look beyond the mainstream headlines and to be able to separate the signal from the noise. In our case, for example, one can find a million analyses and forecasts on gold’s outlook, all highlighting superficial dynamics and featuring simplistic arguments. Monetary policy projections are chief among them, and the narrative goes “Since we expect central bankers to do so and so, gold is projected to react in this way”.

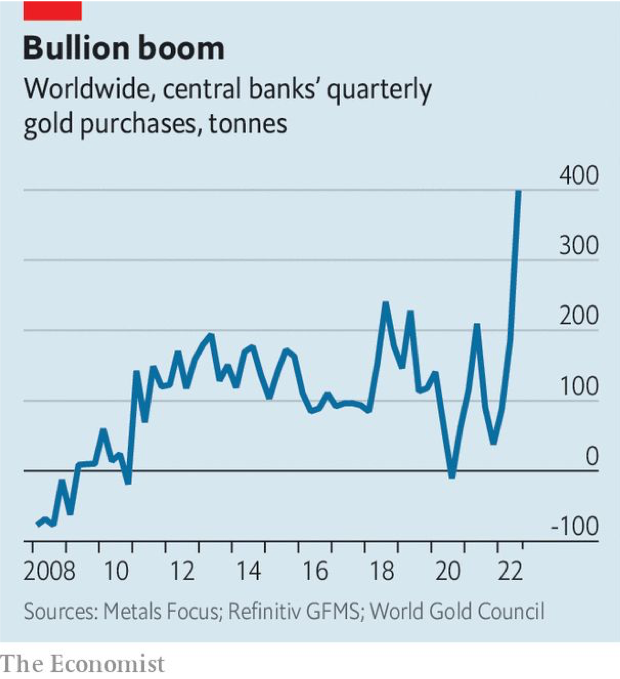

Well, instead of trying to divine the intentions of central bankers, to guess what they’ll do and how it might affect the gold market, wouldn’t it make more sense to look at what those central bankers have actually done, rather than what they say? Cause what they did in 2022 speaks volumes: Globally, central banks accumulated gold reserves at a pace unseen since 1967, back when the dollar was still backed by the precious metal.

Consider this for a moment and then recall all their official statements and projections about the economy and how a recession is avoidable, about inflation and how it’s definitely, absolutely under control and about their faith in their own currencies. Feel free to draw your own conclusions about what’s coming.

Looking forward to the next year, it is clear that there are many reasons to be concerned. The conflict in Ukraine shows no signs of abating and all the preexisting problems it seriously aggravated can also be expected to linger, if not get worse. Inflation is set to continue to plague the real economy, no matter how hard government statisticians try to cook the numbers: Even if CPI goes down, real households will continue to feel the pain. There’s an abundance of supportive forces working in favor of gold and the dynamics are so striking that even the big banks couldn’t help but notice. In early December, Saxo Bank put out an “outrageous” price forecast of $3,000/ounce, in its most “extreme” scenario of a worldwide “war economy”.