by Wolf Richter, Wolf Street:

The seller-buyer standoff.

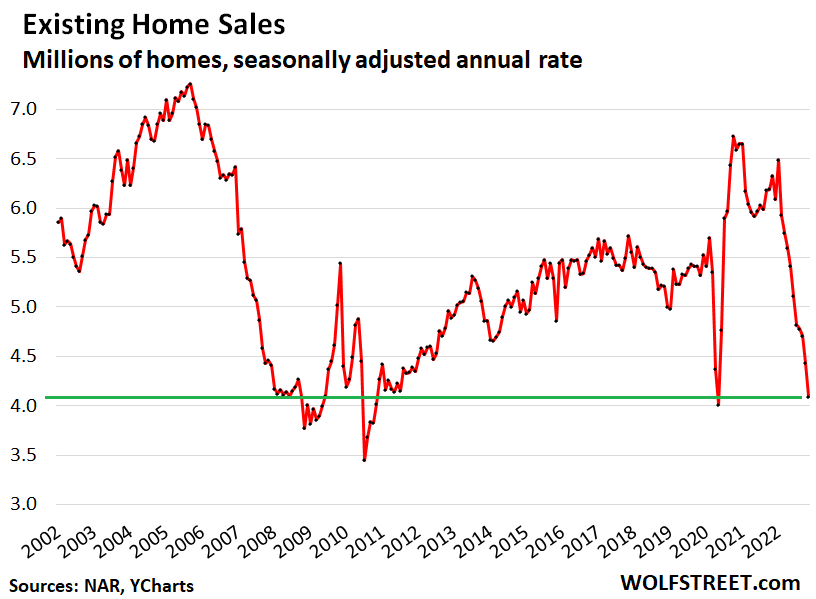

Sales of all types of previously owned houses, condos, and co-ops plunged by 7.7% in November from October, the 10th month in a row of declines, to a seasonally adjusted annual rate of sales of 4.09 million homes, nearly matching the lockdown-low in May 2020. And beyond May 2020, it was the lowest rate of sales since deep into Housing Bust 1, November 2010, according to data from the National Association of Realtors.

TRUTH LIVES on at https://sgtreport.tv/

Year-over-year, sales fell by 35%, the 16th month in a row of year-over-year declines. Compared to the recent free-money peak in October 2020, sales were down 39% (historic data via YCharts):

The above sales figures are “seasonally adjusted annual rates” of sales, so what sales would be like for an entire year at the current rate of sales. Actual sales in November, not adjusted, came in at 326,000 homes, also down 35% from November 2021 (503,000 homes).

Cash buyers are massively pulling back. All-cash sales accounted for 26%, or for about 85,000 homes, of the total 326,000 homes sold in November, as measured by actual sales, not seasonally adjusted annual rate. This was up from a share of 24% in November 2021. But given the much higher number of homes sales in November 2021 (503,000 sales), the 24% share of all-cash sales amounted to 120,000 all-cash sales.

In other words, the actual number of all-cash sales plunged by 35,000 year-over-year, though the share of all-cash sales inched up by 2 percentage points amid plunging overall sales.

Individual investors or second home buyers are also massively pulling back. They purchased 14% of all homes sold, or about 45,640 homes (actual, not seasonally adjusted annual rate), down by nearly 30,000 homes from November 2021 when they bought 75,450 homes (for a 15% share).

Cash buyers and investors are like everyone else: They too see what’s going on in this housing market.

Sales of single-family houses plunged by 7.6% in November from October, and by 35% year-over-year, to a seasonally adjusted annual rate of 3.65 million houses.

Sales of condos and co-ops plunged by 8.3% in November from October, and by 37% year-over-year, to a seasonally adjusted annual rate of 440,000 units.

Sales plunged in all regions, but plunged by the most in the West and the South. Month-over-month and year-over-year:

- Northeast: -7.0% mom; -28.4% yoy.

- Midwest: -5.6% mom; -30.6% yoy.

- South: -7.1% mom; -35.0% yoy.

- West: -12.5% mom; -45.7% yoy.

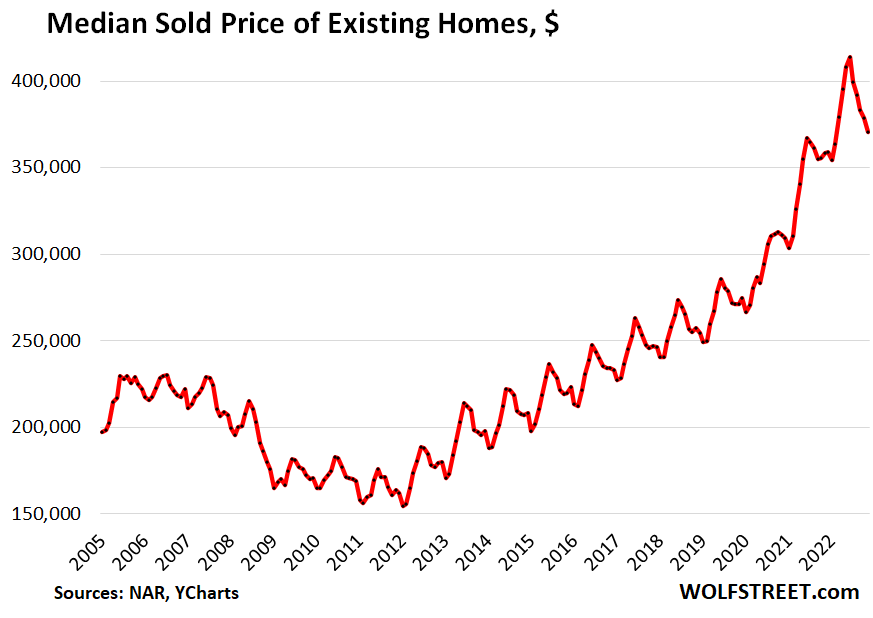

The median price of all types of homes whose sales closed in October fell for the fifth month in a row, to $370,700, down 10.4% from the peak in June. This drop slashed the year-over-year gain to just 3.5%, down from a year-over-year gain of 15% a year ago.

Only a portion of this June-November decline is seasonal. Over the five years before the pandemic, the average June-November decline was 5.8%, with the maximum decline in 2015 of 6.9%. This shows that the current 10.4% decline goes well beyond even the maximum seasonal decline. This is also confirmed by the rapidly shrinking year-over-year price gain, now down to just 3.5% (historic data via YCharts):

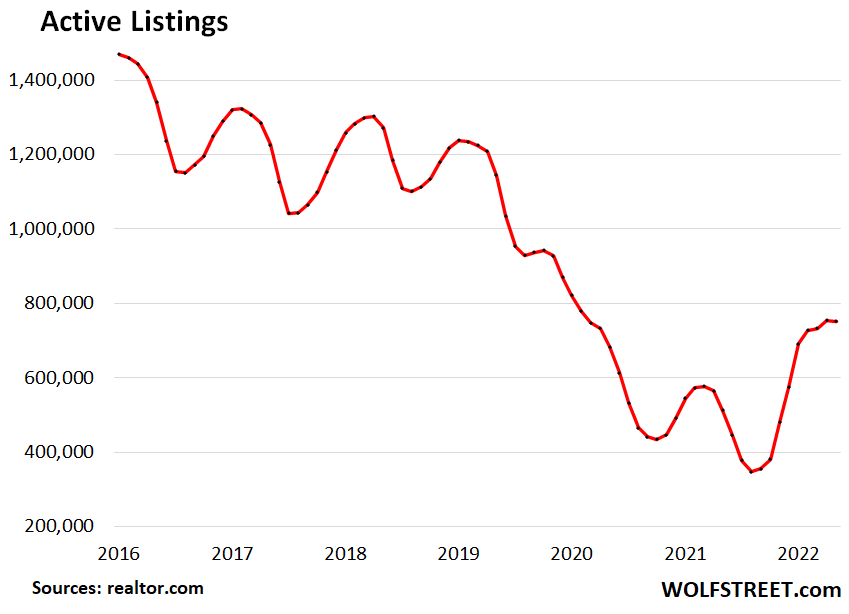

Active listings (total inventory for sale minus the properties with pending sales) were roughly stable with the prior month, at 751,500 homes in November, but up by 47% from a year ago and the highest since August 2020.

Active listings remain relatively low as many potential sellers are praying for a magnificent Fed pivot that will slash mortgage rates back to 3% in no time, and they haven’t put their vacant home on the market because they’re still thinking that this too shall pass; and if the home has been on the market for a while and got no nibbles, they’ll pull it off the market, particularly during the holiday period (data via realtor.com).

Months’ supply in November was unchanged from October, at 3.3 months, both months the highest since June 2020.

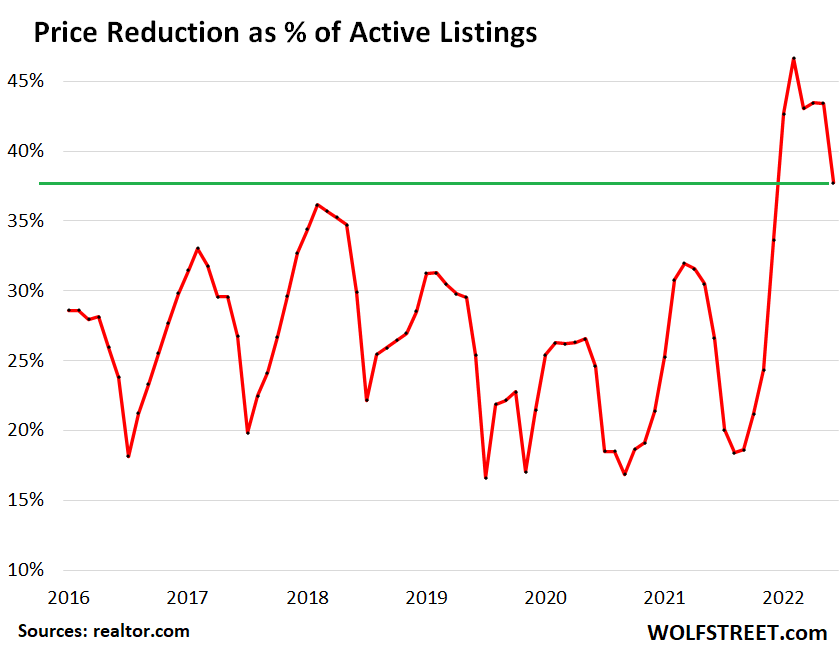

Price reductions: In November, 38% of the active listings had price reductions. While down from the prior months, all of the past six months had a higher proportion of price reductions than any of the prior months in the data from realtor.com going back to 2016 (data via realtor.com).

Seller-buyer standoff: This combination of plunging sales, dropping prices, rising but still tight supply, and a very high proportion of price reductions when homes finally do show up on the market indicates that there is a standoff between potential sellers, who think they’re going to outwait the Fed’s inflation fight; and the potential buyers who have zero appetite for overpaying, with even cash buyers pulling back massively, though they’re not dependent on mortgage rates.